With interest rates rising and housing prices up, it’s no surprise that home affordability is in the headlines. I thought I’d share these two charts that highlight trends in the ‘starter home’ market …

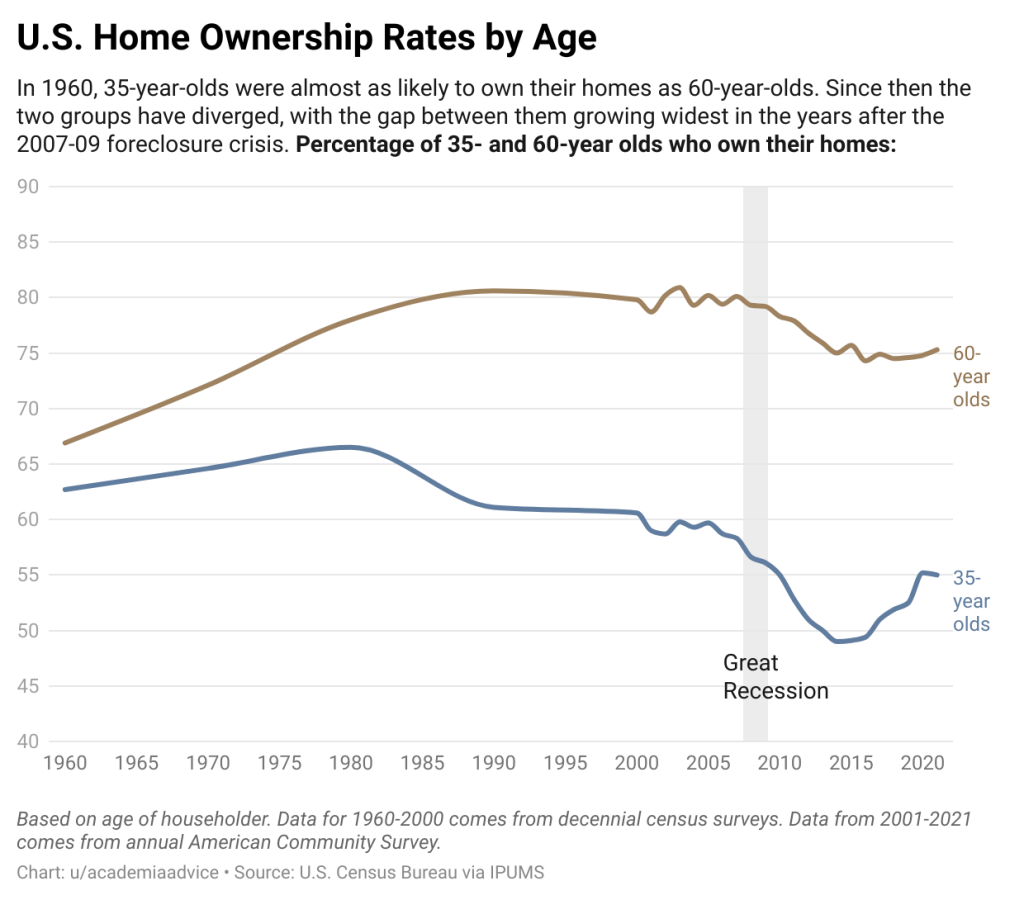

First, this US Census chart is making the rounds as evidence that young people can’t afford homes …

You can see that the gap between 35 & 65 year olds has increased pretty dramatically since 1980. Is this a sign that young people can’t afford houses, or something else?

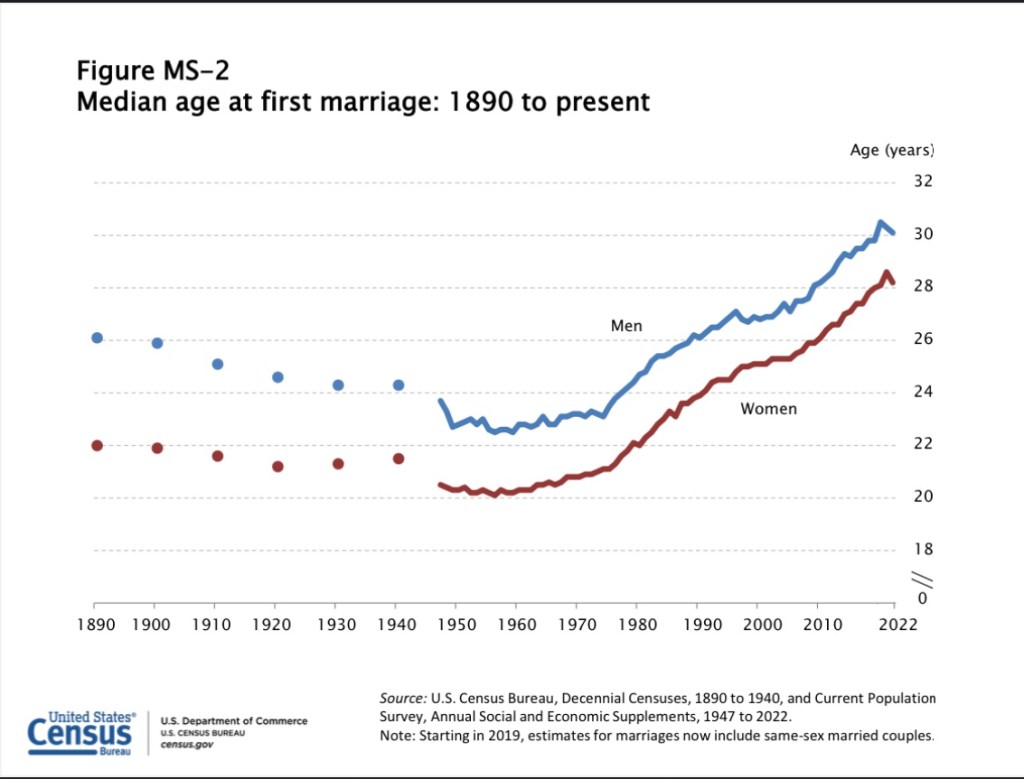

This second chart shows the age at which young people get married (since 1890!). It has also shifted dramatically since the 1980s …

Perhaps what we are seeing in home ownership is that people are waiting to buy a home until they are married. That is increasingly at an older age. After all, why does a single person need to commit a traditional home?

I’m sure there are other trends also shaping this market, but I thought these two charts were pretty interesting to look at side-by-side.

What are you seeing in this market?

Image Credit: Pixabay

There are some Red States where property prices ramped up very quickly during the Covid lockdowns as people moved out of Blue States such as California. This dramatically drove up prices. One of the properties you visited in Florida, Latitude Margaritaville’s prices practically doubled mostly from people escaping NYC. By their standards the properties at twice the price were a bargain. Californians have done the same in Idaho and Arizona. Before that, to Colorado and Oregon.

An auditor for Countrywide, of all things, made a statement to me that California houses never went down in price back around 2006. I remember thinking to myself, where in the hell were you when six houses that touch mine were lost to foreclosure in the 1994 to 1996 timeframe.

In his mind he was justifying the current housing prices because multiple generation immigrant families could afford to pool their resources to buy a single family home. As a contrast, an engineer (who of course is good with math) thought he couldn’t afford to buy a house at the time, but he socked some money away every month to have the funds available when an opportunity became available.

A couple years later, there was the great recession. Those who maintained good credit ratings could buy properties at lower prices with really cheap mortgages. The engineer got a very nice new house for his family. The Countrywide Auditor lost his house to foreclosure.

The key is to save and wait for a house that you would like to live in become available at a price that makes sense. If the prices don’t make sense, then wait for your turn. And, yes houses do go down in price in California and every where else. As parents, it is our job to tell our children that a house may seem insurmountable at the current time. “Your turn will come.” This is where experience of actually seeing this happen a couple times really pays off.

LikeLiked by 1 person

Agree completely! Among the unfortunate elements of the current situation is that more young people didn’t take advantage of the astronomically low interest rates for the last 10 years. That was a huge opportunity for them to lock in when money was cheap.

LikeLiked by 1 person

My observation is that low interest rates drive higher housing prices, because houses are a function of monthly payments. Good buying opportunities happen when high interest rates drive housing prices down. You buy at a high interest rate but cheaper price at a monthly payment you can afford. You can then refinance as interest rates drop to drive down your monthly payments.

I started a series of refinances in 2008 when I got what I thought was a once in lifetime interest rate. Interest rates continued to drop over the next 13 years. I watched interest rates and I was able to refinance without taking any cash out with very low garbage fees that allowed me to earn back the refinance cost in less than year in lower payments. My last refinance was August 2021 at 2.65% for 30 years. My wife and I look at the 2.65% fixed for 30 years as an inflation hedge. Someday after wheeling our wheelbarrow full of cash to the grocery store to buy a case of beer, we just might decide to stop by the bank and drop off a brick of cash to zero out our mortgage.

LikeLiked by 1 person

The topic of “should you pay off the mortgage?” is one of the first I wrote about back in January 2015. https://mrfirestation.com/2015/01/17/living-debt-free-thats-means-the-mortgage-too/

In retrospect, I screwed up that decision for the reasons you’ve been successful. I think rates were about 5% at the time. I probably could have invested those $$$ in the stock market and got a big return. Oh well.

LikeLiked by 1 person

I also see something else in those two charts. A society that increasingly devalues commitment and stability in favor of individualism and mobility. Taken too far, our national ethos of independence can fractionate and subordinate common bonds necessary to sustain our country for the future. When our younger generation delays “settling down” (getting married; making homes), they may not “grow up” into them. We must rediscover the importance of belonging to larger purpose beyond self alone.

LikeLiked by 2 people

Yes – we live in a shorter term and increasingly throw away society. Homes can be great ways to build wealth / especially with tax breaks. I hope they are not missing that.

LikeLiked by 2 people

I see what you describe happening in my neighborhood. We used to have kids running around. As the people got older and sold their houses to younger people, the young people aren’t having children. Time for our country to take a look at itself and ask, why are our most educated young people not have children who become the nation’s future productive citizens?

The only country I hear about trying to turn this around is Hungary, which has implemented family friendly tax policies. Looking back and my wife’s and my time raising children taxes were our highest household budget items despite having high education, food and local transportation costs. I always had a sense that the exemptions for children have fallen far behind inflation and the public schools are not being good stewards with the money we send them.

LikeLiked by 1 person

New WSJ Poll reveals majority of Americans value Hard Work (67% Very Important); Tolerance (58% VI); and Self-Fulfillment (53% VI). In contrast, minority of Americans value Marriage (43% VI) and Community (27% VI). Simply stated, we become what we value, and cease to be what we no longer value. As for Having Children, it’s only 30% VI. The self-fulfilling prophecy here is that this society is in decline, without beliefs, commitments and resources to sustain its programs and bedrock attachments.

LikeLiked by 1 person

I saw that poll, too. My son & I have been discussing it. Patriotism VI fell from 70% in 1998 to 38% today. Yikes.

LikeLiked by 1 person

Yes, the fall in patriotism is profound, but not surprising. Most of the rest of the world neither respects, nor likes us. Neither do we. Another self-fulfilling prophecy.

LikeLiked by 1 person

I told my son that it went even higher after 9/11. That’s why ‘old guys’ like me feel like the culture wars have really sold off something special that brought us together.

LikeLiked by 1 person

Older guys like me know that you’re right, whippersnapper.

LikeLike