Normally at this point of the year I provide an update on how our retirement portfolio is doing against the investment plan we laid out before early retirement. It takes a little time to crunch all the numbers and with the historically horrific headlines we’ve had this year, it might have been easy to just skip the update until later this year.

Still, with the relative bounceback in the stock market and the ‘Lucky St. Patrick’s Day Trade‘ I made two months ago, I’ve been feeling pretty good about how the year is shaping up. Indeed, as I looked at the account balances and put them in my spreadsheet, our portfolio is showing a nice 8% return for the year so far. That’s incredibly unexpected given all that has rocked the markets.

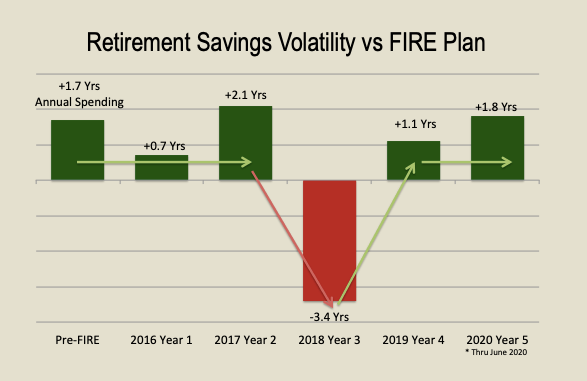

Relative to our original FIRE Plan, we now have almost a year-and-a-half surplus in spending, which is the way I measure how we’re doing …

As you can see, it has not been a steady road for us over the last 5 years, but we’re in the best position we’ve been. The buffer we started with (and lost in 2018) has been completely restored. Despite the impeachment, the pandemic, and the civil unrest, the markets have largely weathered the storm.

So that’s the mid-year 2020 update. We’ll remember this year for a lot of craziness, but happily our portfolio stayed out of the chaos.

How is your portfolio trending?

Image Credit: Pixabay

🍀

LikeLiked by 1 person

Ha ha. Of course the day I post this, DJIA drops 900, CV19 starts going up again, and the Fed dampens their outlook. Oops.

LikeLike

“Life is either a daring adventure or nothing at all.” — Helen Keller

LikeLiked by 1 person

2020 “Adventure Time” 😆

LikeLiked by 1 person

I’m in the situation where I am contemplating FIRE in the midst of the turmoil. I have been debating a date a few days before my 55th birthday in October, or just after the start of the new year . I have days where I don’t even want to look at the markets (3% market drop yesterday). Although I think that the numbers are solid, I dread the doomsday scenarios of markets dropping 30-50%.

Our current plan is for me to retire first, while my wife continues working for at least a year or two more. I have been using firecalc, and looking at both 4% and 3.5% rates of withdrawal which put me safely 10-20% over current salary. I am also in the unusual situation of having inherited a sizable IRA last year under the new tax law that must be fully distributed within 10 years. Everything looks like its affordable, but making the leap is daunting.

We are in good shape financially and it seems we have enough in my retirement plus investment income to cover all of our household expenses plus, but the uncertainties of the market have me worried that I am going to retire and then see the market suddenly drop 30%. We are generally frugal, and had to adapt from two salaries to one during the last crisis without major harm. How much uncertainty with the current situation is too much?

LikeLiked by 1 person

Times are as uncertain as I can remember with an impeachment/election year, global pandemic, economic lockdown, and civil unrest/race riots. Yet, despite this past week’s sudden downturn, the markets haven’t cratered. It sounds like you are sensible with your money and have a buffer above what you need. That being the case, I would say the extra money you gain by continuing to work are probably not worth as much as the time you buy by early retiring. We all have more than we need by any global standard. Most of us have more than we ever expected. As a result, ask yourself “isn’t time the ultimate luxury?” Or, do you really need more stuff?

LikeLike