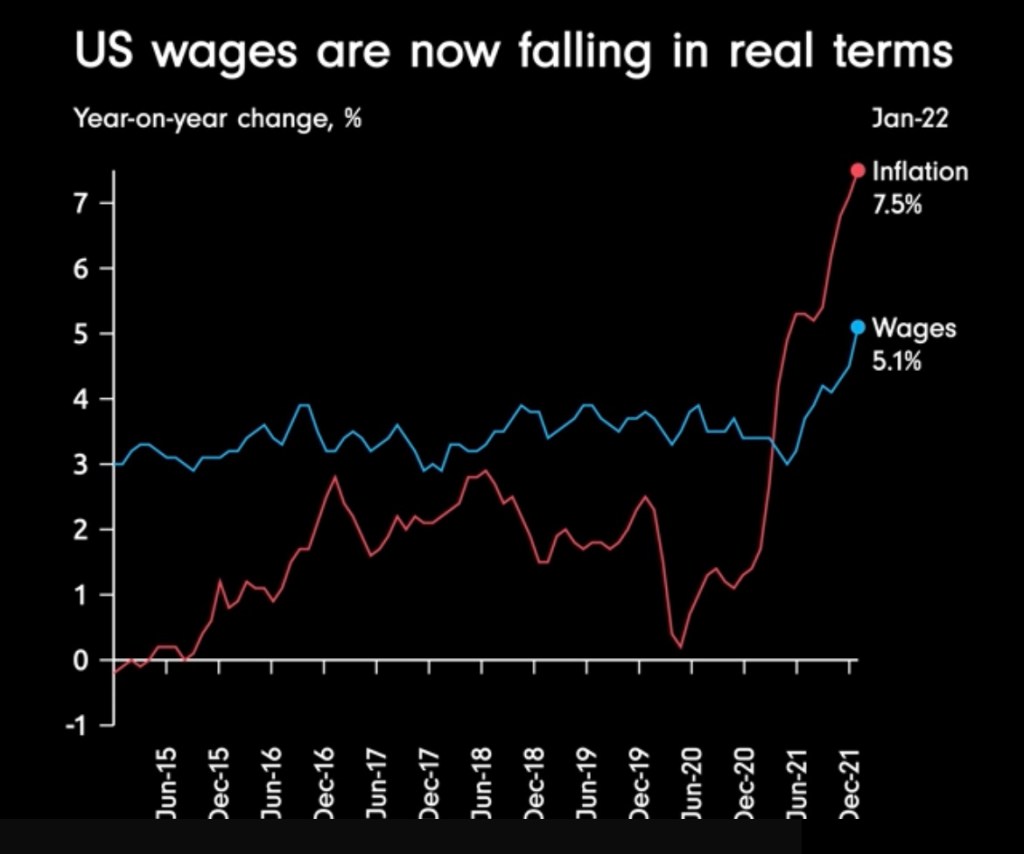

If you are working, you might as well take off an hour early on Friday. As you can see from the chart, wage growth is now lagging price inflation. The 2.4 pt gap equals about an hour’s work against a 40 work week.

I’m guessing millions of younger workers are coming to the hard realization that wages don’t generally keep up with rapid inflation. Employers tend to index wages to what other businesses are paying, not how much cars, houses, energy, or healthcare cost.

The gap to inflation is also influenced by technology. If wages get too high, businesses are further encouraged to digitize or automate. The costs for software and robotics drops every year, putting the squeeze on pay increases businesses need to provide.

When I look back at my career, I see that almost all of my wage growth versus inflation came from promotions. Sure, I had years when I was 2-3-4 pts above inflation, but I also had years when my merit increase didn’t keep up. I even remember a couple bad years when MegaCorp just froze everyone’s pay outright. That wasn’t good for morale, but big surprise … MegaCorp continued on.

My advice for folks early in their career is to just focus on reaching the next rung on your career ladder and ignore what is happening with your annual raises relative to inflation. Promotions will boost your income 10-20-30% in a single jump and make annual merit increases look immaterial.

Besides, if you are effectively positioning yourself to move up, you are probably getting higher than average annual raises already.

How much of a role did annual increases play in your journey to FIRE versus promotions?

HAVE A GREAT WEEKEND …

Image Credit: Reddit r/dataisbeautiful

An interesting exercise to see when you were getting ahead of inflation and when you fell behind is to logon the Social Security Administration’s Website and download the longform benefits calculator, where you can look at your earnings statement and have to manually punch your yearly numbers in. This longform calculator shows roughly your annual earnings and has a column that indexes the individual years for inflation. I used the qualifier roughly, because there were years when I exceeded the SS Maximum ‘contribution’ by a lot and the income before Medicare became uncapped doesn’t show up.

My career lacked a steady progression, as a started my career as an engineer, spent most of the time in sales, and ended by running IT for a company, and finally retired and got involved in consulting. My earnings were quite lumpy, which actually in a way was a blessing. I will outline by decade roughly what happened and why I call lumpy earnings a blessing.

1980’s – Started with me working as engineer, going into sales halfway through and earned $120,000 in 1989. This was a lot of money back then. Social Security Taxes including Medicare maxed out at $48,000. You could and I did buy a couple acres in Malibu for a little over $100,000. I moved a trailer onto the land and built my own home to keep the cost down. This was a great financial move.

1990s – The early 90s were horrible in LA. Due to the Soviet Union falling, defense budgets dried up and what was left packed up and left town. Six properties that touched mine were lost to foreclosure.

I got married in 1994, and my wife and I lived on one of our paychecks and saved the other income through a combination of maxing out two 401-Ks with employer match and putting anything leftover into individual stocks.

The end of the 90s were my all time high water mark in terms of earnings from working. I was at a company where I achieved the highest sales out of 500 salespeople and had baseball player type earnings. My wife and I only touched my base pay after maxing out a 401-K with company match, and a discounted employee stock purchase plan, which I also maxed out of course. 50% of my commissions were contributed to a Deferred Compensation Plan and the rest was used to invest in individual stocks.

2000s – The all time great job ended after the first quarter of 2000, when the company was sold to a company that wanted to cut paychecks. Mine being one of the largest was one of the first to go. The early part of decade was so-so. I ended the decade at start-up where I introduced mass emailing for sales prospecting coupled with webinars. Using this for my sales territory actually got my sales production to surpass the other five territories of the company combined. Of course my wife and both maxed out our 401-K’s with company match, and bought individual stocks with any extra money we had leftover. Guess what happened to that company? You are right if you guessed it got sold.

2010s – I ended up at the company that I stayed at the longest. I didn’t make great money. My wife and I maxed out 401-Ks with a match as much as we could. Ironically I got moved back into running their IT and actually fell behind inflation. Just sort of lost in the back room.

I also made a great investment discovery in 2010. I could buy stocks of stable companies like Home Depot and Microsoft that had over a 4% current yield on their dividends and were growing the dividend over 20% annually for HD and over 10% annually for MSFT. I thought of this plan as a way to have dividends that you can live on, and the increases will keep you ahead of inflation. I highly recommend seeing what happens when you take a 4% dividend and grow it around 20% annual with reinvestment over ten years. My son actually ran these numbers for a school project where the teacher wanted his students to learn about the wonders of compounding. When the teacher saw the numbers, he actually thought my son made a mistake until he ran the numbers himself.

I retired in 2020. Remember that Deferred Compensation Plan where I put 50% of my commissions into back in the 1997 to 2000 timeframe. Compound that over 20 years and it has replaced my income from working. My wife and I are also living off dividends from individual stocks we bought over the years that are held in a brokerage. We aren’t touching our 401-K’s that were rolled into self-directed IRAs yet and plan to not start Social Security until we each hit 70.

Remember I mentioned that lumpy earnings were a blessing. My wife and I did not go out and spend any windfall earnings because we didn’t trust that they would last and they didn’t. We kept our expense base low and invested any extra we had. This helped us retire younger than normal with more income than normal, despite having an income from working that fell behind inflation.

LikeLiked by 1 person

Great story, Klaus – thanks for sharing the whole thing. A couple things pop out at me:

1) Sales people can make a boatload of money. They really make it rain for most companies and their compensation is based on how well they can do. Just like the pro athlete salary you mention, it is easy to exactly measure what sales people contribute.

2) The back room folks frequently get forgotten. Whenever possible, get yourself in a ‘line’ function instead of ‘staff’ function in any company. The jobs are harder, but pay the real rewards.

3) Don’t live your company, it will never live you back. In fact, if there are cutbacks or an acquisition, sometimes they will cut the very people driving their success. It doesn’t make sense – except to a company accountant.

4) Bank your raises, bonuses, and defer money for later. Hardly anyone does this, but it’s the real secret to reaching FIRE. If you think it’s hard to not spend you money immediately, you need to remember you’ll still get to spend it later.

5) Lifestyle creep kills people financially. If you can be happy in your 50s with the lifestyle you created in your 20s/30s … you will be happy your whole life.

One question … do you still have the land / place in Malibu? That has to have appreciated a ton. If so, it’s no wonder you are content in California – Malibu is such a great area!

LikeLiked by 1 person

Yes, I still am in the place I built in Malibu. My wife and I have never taken a cent out of the house either. We could easily pay it off, but like the inflation hedge offered by 2.65% 30 year fixed financing. Some day when I am wheeling my wheel barrow filled with cash to the grocery store to buy a case of beer, I might just drop a brick of cash off at the bank to pay off the mortgage.

I think you hit the nail on the head when you summarized the secret to our success was avoiding lifestyle creep. Lifestyle creep and treating the equity in their homes as a piggy bank caused six of the houses that touch mine to get lost to foreclosure around 1994. Seeing what happened to our neighbors and being subject to being laid off about once per decade served as a constant reminder to stick to our frugal living plan. We wanted to live the opposite of the all hat, no cattle lifestyle.

Here is a story from the company that I was working at in the late 80s. I was making more than the other sales people at the company and was starting to get a target on my back, along the lines, “How come that towny from Wisconsin is making more than everyone else?”

The CFO actually ran Cost Benefit Analysis on the sales team. I had the same fixed costs as the others consisting of base, benefits, and car allowance. When you added the fixed employee costs to commissions and divided the sum into the amount brought in, my cost of sales was the lowest. The highest cost of sales was the person who was barely getting by.

LikeLiked by 1 person

Here are some numbers that shows how incomes fall behind inflation.

Government’s advertised Inflation Rate in 2021 was 6.8%.

The average corporate pay raise in 2022 is 3.9%.

Security Security 2022 COLA is 5.9%.

The loss to inflation is actually much worse than the difference between the advertised Inflation Rate and your pay increase when you factor in taxes. Remember taxes are the highest household budget item for most who are reading this forum.

Social Security COLA was 5.9%, yet Medicare Part B Premiums increased 14.5%.

The Standard Deduction for Married Couple Filing Jointly increased from $25,100 to $25,900, which is a 3.9% increase.

Here is a comparison between 2021 and 2022 Tax Brackets for a Couple Filing Jointly.

Bracket 2021 2022 Increase

10% 19,900 20,500 3.0%

12% 81,500 83,550 2.5%

22% 172,750 178,150 3.1%

24% 329,850 340,100 3.1%

32% 418,850 431,900 3.1%

35% 628,300 647,850 3.1%

37% >628,300 >647,850 3.1%

Other areas of the tax code provide absolutely no relief from inflation. For example the Maximum AGI for the American Opportunity Tax Credit stayed at exactly $160,000, before the phase out kicks in.

Here is my analysis of these numbers. Most Americans know that they are experiencing a decline in their buying power because 2022 income increases have not kept up with the Government’s advertised 6.8% inflation rate. The loss of buying power is actually much worse than the difference between your income increase and the government’s advertised inflation rate because the Standard Deduction and tax brackets are not properly adjusted to offset inflation. The loss to taxes is further exacerbated if the additional income that doesn’t buy as much causes one to trigger tax credit phase-outs and Medicare Part B premium increases.

My final comment about why I called the 6.8% Inflation Rate, the Government’s Advertised Inflation Rate. I think last year’s true inflation rate was closer to 14.5% that the Government raised Social Security Part B Premiums by this year. It is funny how Governments get the inflation rate right when it comes to paying themselves.

When I analyze my income over time, I can see the loss of buying power to taxes. Back in the late 80s I was able to really get ahead. Taxes were not my number one budget item back then and my money seemed to go a lot further. The government has been lying to us for years about the true inflation rate by leaving out higher education, housing and taxes which are some of the biggest cost drivers for middle class families over the past 40 years.

LikeLiked by 1 person

Very thoughtful analysis, Klaus. If the average person put any energy into the number of ways the federal government is gaming their own system, we would be writing a new constitution tomorrow!

LikeLiked by 1 person

Slightly over half the people are net beneficiaries from government spending and think they are going to get a free ride on the backs of ‘the rich’ who often are simply the upper half of the middle class. Inflation is a tax against everyone, but it hits those the worst who have the tightest budgets. They are the ones who will not be deciding whether they fly to Hawaii or drive somewhere local this year for vacation. Their choice will be do I heat or eat?

LikeLiked by 1 person

Yep. At a federal level, more than half pay zero income tax, but they can’t avoid inflation … https://www.businessinsider.com/more-households-didnt-pay-anything-in-federal-income-taxes-last-year-2021-8

LikeLiked by 1 person

I don’t think the Constitution is the issue, with these exceptions.

1) A Constitutional Amendment that limits that percentage of GDP that the Federal Government gets to spend.

2) A Constitutional Amendment that requires the Federal Government to have a balanced budget to force it to live within its means.

3) Give the President a line item veto. More on an opportunity that Trump missed in this area later.

4) End the ability for lobbyists to donate (bribe) politicians. This prohibition includes public employee unions.

5) Disallow government workers and their family from investing in anything other than mutual funds offered to all government workers.

Of course the corrupt politicians would never go for this. It would hurt their ability to make millions working at a job that pays around $170K per year. My answer to this is we the people need to build a wall around Washington D.C. and turn it into a penal colony.

Here is where Trump really missed an opportunity to operate as if he had a line item veto. He could have gone through the budget that Congress submitted, made red line changes, just like we do to contracts, initialed and dated each change, and signed the budget with the instructions that Congress was free to initial, date and counter-sign the red line changes.

And, if they refused to execute the revision, he could have used his bully pillory to publicly shame members of Congress by shining a light on the stupid pork they have in their budget.

LikeLiked by 1 person

I could agree with most all of those amendments. That is, of course, a pretty big change to the nature of the federal government at this point.

LikeLiked by 1 person

Pay freezes? I wish it was only that. I worked for local government no COLA and we actually took pay cuts 5% two years in a row while the portion we paid towards our pension increased. This while police and fire unions got raises! Theoretically we could take extra time off, but dedicated management such as myself had pride in getting results, the work still had to get done. I’m certainly glad to be gone from that place. Overall I really enjoyed the work and when factoring benefits including pension I am happy to have worked there, but those there now given Covid have it rough.

LikeLiked by 1 person

It’s definitely hard to keep up with inflation when you take a pay cut! I’m guessing that’s pretty unusual for anyone who works for the federal government or a big MegaCorp. But local government, start-ups, small businesses, and certainly folks that work for themselves go through that often. In addition, anyone over 35 who has ever been laid off has likely taken a big pay cut or two in their career, as well. Forget keeping up with inflation in those situations.

LikeLike