I’ve been worrying about periods of high inflation since I started writing these posts over seven years ago. It wasn’t until these last 12 months that my worries were matched by reality.

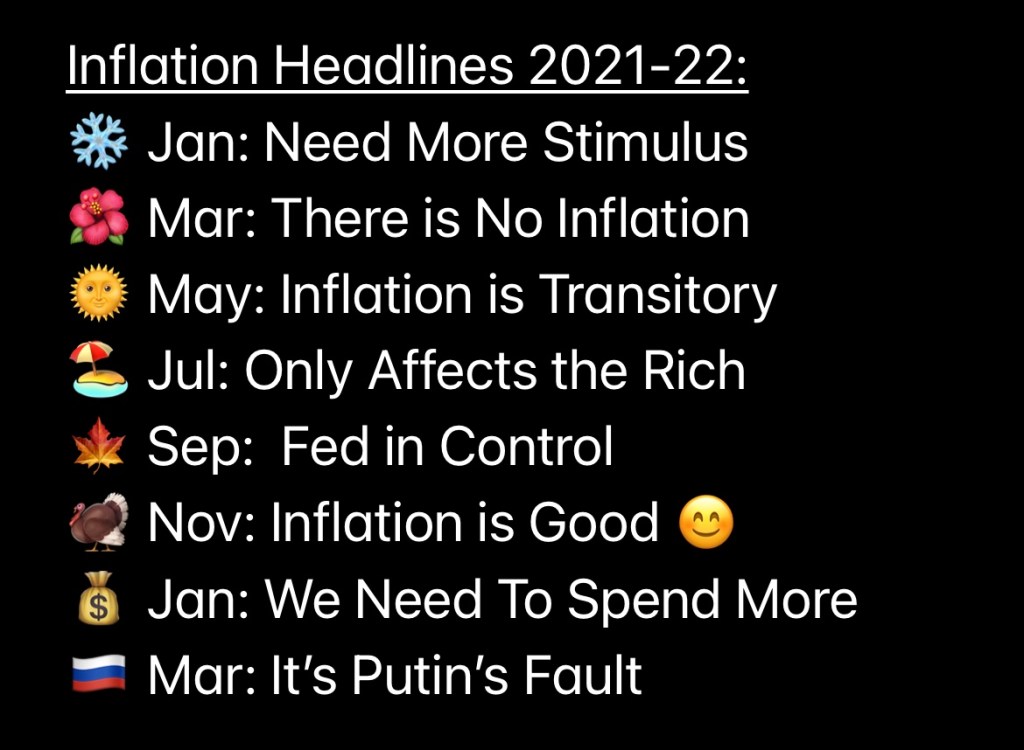

It doesn’t help that the politicians & media pundits keep trying to put a positive spin on things. The headlines have been ridiculous:

Part of the challenge is I don’t know if the inflation measures themselves are even accurate.

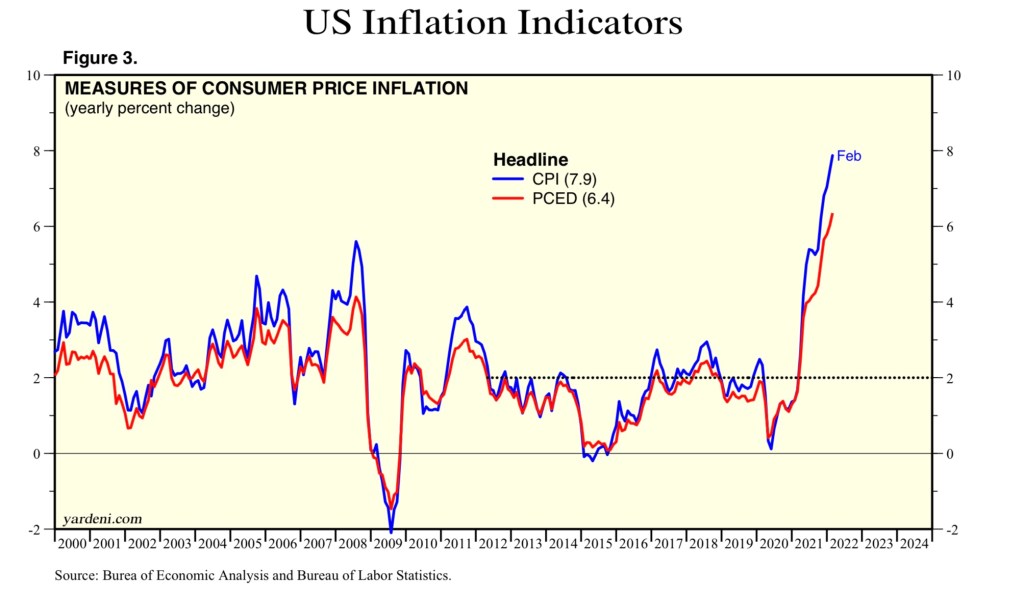

Prices ‘feel’ like they are much higher than the official CPI of +7.9% versus year ago to me. That’s not scientific, of course, but I’ve never been sure we can trust the government is giving us the straight story on how much the dollar is losing in purchasing power.

I also don’t have a good alternative.

Since the mid-2010s, the Federal Reserve has emphasized the ‘Personal Consumption Expenditures’ index (PCE) as their preferred measure of inflation. They say it’s more accurate, but It’s grown at a slower rate than CPI: +6.1%. Still, the PCE is also the highest numbers since 1982.

The ‘Producer Price Index’ is another alternative. It’s up more than CPI: +10.0% in February. That feels closer to what I am seeing at the store and at the low-end of what I am hearing from organizations I’ve been involved with (corporate & non-profit).

It doesn’t help that the government has used different formulas to measure inflation. There is a website called ShadowStats.com that purports to share CPI numbers using the formulas the government used prior to changes in 1980 and 1990. They are calculated more conservatively now than in the past.

ShadowStats shows the current CPI over +15% – even slightly higher than the early 1980s. Some economists claim that was a better way to measure inflation, but others say the measures needed to change.

If we take all of these numbers together, I guess we could say we have a likely range of inflation from +6-15% right now. I’m thinking we are closer to the midpoint of that range (~8-9%) than the low end (which the Fed is using).

Like the weather, I can’t do anything about inflation but I still wish we could agree on what the temperature is!

What is your read of inflation right now? Do you trust the government’s measurement?

Image Credit: Pixabay

My read: Inflation bad. Cruelest tax of all. Government prints gazillions they don’t have. Government benefits from inflation; people don’t. Government points fingers at everyone else but themselves. Government remains in power. People remain cowed waiting for government to solve inflation. That is like waiting for the arsonist to quench the fire. Do I trust the government? Not any farther than I could throw them out of office. What fools we mortals be.

LikeLiked by 2 people

The government’s fake inflation rate was 7.9% over the past 12 months. Yet the Social Security COLA for 2021 was 5.9%. Most wage increases were are 3%. I agree with Chief’s assertion that the true rate of inflation was around 15%.

While preparing my taxes this year, I took a couple minutes to check the tax tables for 2022 and found that the standard deductions and brackets were adjusted up by around 3%. Some of the tax code phase outs are not indexed for inflation. The phase out for Social Security becoming taxable has not been changed since 1984. The end result will be if you manage to increase your earnings to keep with up with inflation, you will keep much less due to taxes not being properly indexed for inflation.

As a parting comment, Washington, D.C. doesn’t produce or invent anything, and yet six of the ten richest counties in the country are clustered around the DC metropolitan area. The civil serpents are getting rich off our hard work.

Let’s hope that people have an understanding of why they are having trouble affording necessities such as food, housing, gasoline, and home heat for the upcoming November election cycle.

LikeLiked by 1 person

To put that change in the standard deduction income brackets (+3%) in context, the “wages and salaries for all civilian workers” (BLS data) ‘shows a fast 4.4 percent annual rate in 2021”. That’s a silent tax increase of 1.4pts on everyone.

LikeLiked by 1 person

“What fools we mortals be” … Shakespeare wrote that line in 1595. The government of his era, the reign of Elizabeth I, was even worse than ours. Maybe in a few more centuries we’ll have something better.

LikeLiked by 2 people

For 2021, Social Security COLA was 5.9%, which is close to the false inflation rates advertised by our government. Yet, they raised Medicare Part B premiums by 14.6%, which is remarkedly close to your 15%. They are gaming the numbers by picking a basket of goods that does not include necessities to live and are some of the major cost drivers right now.

The timing is ripe for another Contract with America. The Scott Plan is heading in the right direction.

LikeLiked by 1 person

I like a lot of what is in the Scott Plan, but given the reception it has gotten in the media, I’m not sure it is a good political idea for the minority party to promote it. It worked for Gingrich, so I could be wrong. Politics is tough to predict.

LikeLiked by 1 person

The “everyone have some skin in the game” point is a non-starter. Gingrich did a better job explaining his policies so that the normal everyday person could understand it and politicians could align with them and run with the mandate that they would support it. For this cycle, inflation, gasoline, school choice, the border, keeping this USA out of wars will resonate.

LikeLike

I fear, that we are all in for a rude awakening. The long term affect of double digit inflation will be devastating for many longer term portfolios. As a young child, I can distinctly remember my dad and uncle discussing how anyone had it made, making $200 a week. It seemed like so much money! Gas was $0.40 per gallon, $30 would buy a weeks worth of groceries, and a brand new family car was about $3000 at that time. All of those costs still seemed exorbitant to most families, but it was about to get much worse. My uncle was discussing a “huge” lump sum pension payout from his company to retire early of around $250k. He was going to be on easy street…he would gleefully tell my dad. My uncle lived to be 90, and let’s just say he was not a wealthy man in retirement. Inflation was devastating through the 70’s (and well into the 80’s), and it ruined many retirement dreams…like his. Most people today have never experienced that “hidden tax” pain. I fear without significant changes in our fiscal direction as a nation, we may be about to learn the hard way (again). Let’s hope I’m wrong, or even better, that we wake up as a nation and make some significant spending changes. You can’t continue to print unlimited amounts of money forever. You can’t give trillions of free stuff to work-capable citizens and have them sit home instead of contributing to society. You can’t frivolously spend your way into unlimited debt without an eventual reckoning. Eventually this will all come home to roost, and it has likely already begun. Those of us with assets will now pay those bills via the “hidden tax” whether we know it or not. (Let’s hope I’m very wrong.)

LikeLiked by 2 people

I agree with you 100%. The only fixed investment aid have is my MegaCorp pension. I guess that will get devalued in purchasing power much quicker than I expected. We also carry a few years cash ‘cushion’ – I might have to invest a bit more of that before it gets devalued. The rest of our wealth is in equities & real estate, so the biggest part of our portfolio (by far) will be fine.

LikeLiked by 1 person

My GrandFather retired at age 50, and lived to 96 without running out of money. He invested in stocks of local companies in Pittsburgh, PA consisting of mostly banks and utilities companies. The key was he was living off dividends from boring stable companies that were not fashionable. The dividends increased every year. He was retired long before the 70s and made it through just fine.

He was buying stocks during a time when information was harder to come by and transaction costs were very expensive. People signed up for DRIP plans that required them to actually hold physical certificates. Companies acquired stable investors who were more partners than stock flippers. Shareholders often invested in local companies, because they had an information advantage and often attended shareholder meetings.

I am teaching my sons now, to do the same. They are starting earlier and have learned that investing should be a boring math based process.

LikeLiked by 1 person

My grandfather was from Pittsburgh PA, too. North Braddock, actually. He moved to WI at an early age, but continued to invest time & money in the Pittsburgh Steelers & Iron City Beer! 😉

LikeLiked by 1 person

My grandfather lived in Penn Hills. I was born in Wilkinsburg, which splits the difference between Braddock and Penn Hills. Have you been to Pittsburgh recently? They have really cleaned up the downtown and the air is much cleaner than it used to be in the 70s.

LikeLiked by 1 person

We used to go to Pittsburgh a lot when I was a kid to visit distant relatives. That was in the 1970s. We’d go to Kennywood when we were there. I went back about 7-8 years ago when I was speaking at a conference at Penn State. Only had a little time to drive around. Tried to find my great-grandparents house, but North Braddock is quite a mess. Found the street, but couldn’t find the exact house.

LikeLiked by 1 person

Yes, Kennywood, with the Big Dipper. Their old wooden roller coasters were a very rough ride.

My grandfather had a nice house in Penn Hills on a couple acres of sloping ground, and he built his house himself (sound familiar). He had an planted an apple orchard, had lots of grape vines, and a large garden that he planted during WWII and just kept going. I looked at his property a couple years ago on Zillow and it was worth a relative pittance. One thing your can try is looking up properties where you lived or one of your relatives lived on Zillow. Go to the bird’s eye view and you can walk virtually around the neighborhood. You will be amazed by how small your free range roaming ground was. It is also a bit of brain teaser trying to walk yourself to school on the app with a first person perspective.

LikeLiked by 1 person

Yeah – I’ve done the Zillow / Google Maps walk. The challenge is his family moved away in the early 1920s (to Wisconsin). We only have a couple black & white pictures of their house as it looked way back then. All of the houses have changed a lot in a hundred years and many are gone. I got it narrowed down to 3 houses when I was there. Hope to figure it out someday, but not worth a ton of time to start looking into old city records.

LikeLiked by 1 person

Here is some follow up from helping my middle son do his taxes. Yes, I do them myself, so that I can understand the cost drivers while looking for potential to have the government steal less of your hard earned money.

Previously, I had posted that their were certain income bands where government can steal 66% of each incremental dollar of someone who would still be considered high middle-class. Well today I stumbled upon a scenario where the government theft actually equaled 94.5%.

Here is the scenario:

You have a Married Couple who are earning $160,000. They think that sending the wife back to work to bring in another $12,000 will give them some discretionary income to go to send their children to Catholic School or allow them to lease a Maserati, or whatever.

For this scenario we have a married couple, with both on Medicare, they have a child in college and they have $10,000 in annual income from tax free municipal bonds. Here are the incremental taxes on that extra $12,000.

Missing out on 3rd Stimulus Payment – $2,800

Missing out on the majority of AOTC – $2,115

Federal Tax @ 22% – $2,640

Social Security ‘contribution’ – $744

Medicare ‘contribution’ – $174

CA State Disability ‘contribution’ – $120

CA State Income Tax @ 9.3% – $1,116

Total Government Taking = $11,341

Government taking as a percentage $11,341 / $12,000 X 100 = 94.5%. I added Medicare Part-B to push the number as high as I mathematically could. Without Medicare Part-B, the taking would have been only 80%.

Of course let’s go Brandon’s voter are complaining that we are not paying our fair share.

Here is the other takeaway from going through my taxes with my son. He was embarrassed to send me a copy of his brokerage 1099. It turns out he invested in some Chinese crap stocks, based upon some hot tip that one of his friends gave him and lost $10,000. Then he panicked and sold a bunch of good stocks that I provided for him and went into cash.

This was teaching moment that I hope sticks with him the rest of his life. Invest in boring and stable stocks with a reasonable dividend yield, that are growing in businesses that will be here for the long term. Do this for 20 to 25 years, so your dividends will take care of you. He is learning this lesson earlier than me at age 25, and much earlier than his twelve year older brother. Next year he will follow the program.

There is goodness in understanding your own taxes or helping your children with theirs. It is a shame that the civil serpents in our government think is is acceptable stealing $11,341 out of an incremental $12,000 in income. This comes from thinking along the lines, they have a lot and we need to help this group of people.

LikeLiked by 1 person

I have to confess, I had an incorrect remembrance about Kennywood. The largest wooden roller coaster was Thunderbolt. That thing scared me a lot when I was young. Metal roller coasters just don’t make the same amount of noise and jerk you around the same way, even when they are going upside down.

There was another little roller coaster called the Dipper.

LikeLiked by 1 person

I was pretty little when I was there. I don’t remember coasters. I just remember the Noah’s ark, Go-kart/speedway, and the log flume. It might have been the first amusement park I ever went to. We probably went 3x on different vacations.

LikeLiked by 1 person

Krause,

I also was stunned at the “extra” cost for Medicare due to high income,that is onerous. I was against the stimulus but it isn’t an extra tax, but welfare for middle income to low income people. I agree that at a certain point in time disability tax should disappear. The other “extra” taxes I have no issue with.

I did get a $32 penalty for 2021 as I earned more from consulting in retirement than expected thus my quarterly payments were insufficient.

Now don’t get me started on gas tax rebates, student loan holidays, eviction holidays, and the piece de resistance, paying family member as caregivers. Only in our state of California!

Yes, we pay high taxes which I don’t like. I call it the paradise tax. I would hate to live in Florida, Texas, Arizona or Nevada

LikeLiked by 2 people

One of my coworkers before I retired, called the approximate 10% CA State Income Tax, “Tithing to the Sun God.”

My point was that a couple making more than $160,000 did not get the stimulus. My son qualified, and it ended up on his tax form as a tax credit. There are certain income levels where you are better off staying home instead of busting your butt to go to work, because you will not net that much more incremental income.

In my scenario, the majority of the damage was done by the Federal Government. Some of the other states you mentioned have some hidden costs of their own. TX has Real Estate Taxes that are around 3% and are not capped at an up to 2% ‘maximum increase’ per year. Some areas of FL have very homeowner’s insurance due to the hurricane risk.

California has been where we are now in the early 70s. People finally had enough and the result was Proposition 13 and the Reagan Revolution. I think we are getting close. This time around solving gasoline / energy high cost, crime, school choice, homelessness, and the lethal drugs that are pouring over our border is an attractive package.

LikeLiked by 1 person

Yes, MN has the “paying family members to be caregivers” program too.

LikeLiked by 1 person

Remember those business strategies from the olden days: Grow, Maintain, Sell, Milk? We are being milked.

LikeLike

Great analogy! Definitely being milked. 🙂

LikeLike