I just read an interesting study on the risks & worries of retirement. That is, what do people worry about happening in retirement compared with what are the real risks?

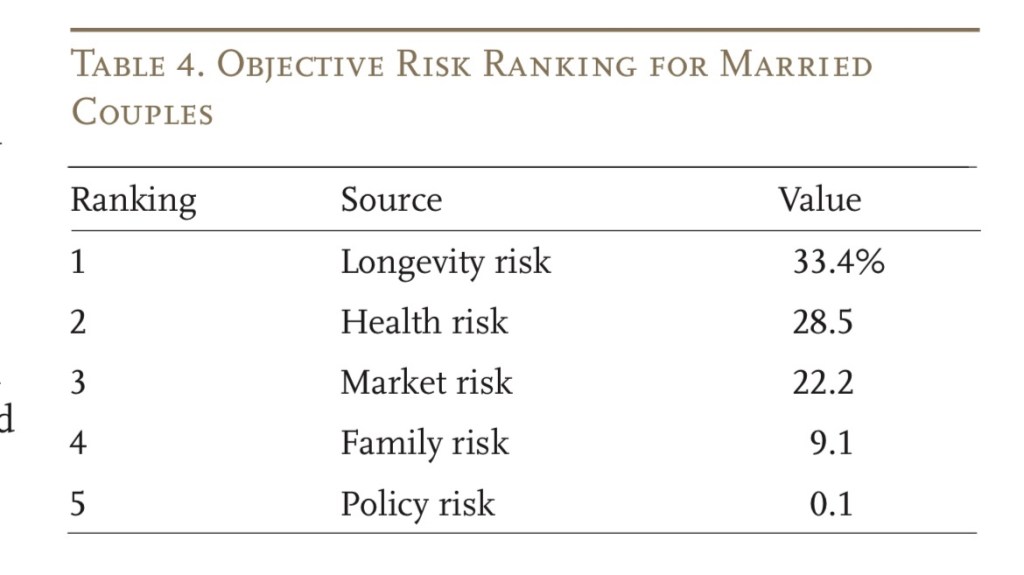

The news is good. Even though the volatility of the markets going up & down make the headlines each week, the actual biggest risk is living longer than you expect:

Living longer than you expected should be good news, shouldn’t it? The downside is if you don’t plan to live that long you may have already tapped out your retirement nest egg.

The second key risk is ‘Health’ – that is having a major medical issue with very expensive treatments needed. Deductibles are higher than ever, policies don’t cover all treatments, and out-of-pocket expenses can add up quickly.

‘Market’ risk – which relates to significant drops in investment value – comes in at number #3. Most people in the study’s survey believe this is their top risk, but it’s not. As I’ve shown before, longer lifetimes can result in bigger portfolios …

Related: How Long Can FIRE Last?

The bottom two risks are just a fraction of the others. ‘Family’ risk means a divorce or needing to support a family member. And, ‘Policy’ risk involves changes to government entitlements or tax rates.

What retirement risks do you worry about the most?

Image Credit: Pixabay

Good Morning Mr. Firestation, thanks for highlighting this article. I was actually confused when I read it earlier this week. I don’t understand how long term market risk and longevity risk are not the same thing. Take something simple like the 4% guideline, combine with a low cost 80/20 long-term investment strategy, then run a monte carlo simulation. I believe the results will show a portfolio that never runs out of money at least 50% of the time. So, if you do run out of money, it was the result of lower probability below average market returns and/or sequence of returns. Right? Aren’t those actually market risks? Thanks again and have a great weekend.

LikeLiked by 1 person

My read of the study is that it just assesses the likelihood of facing a down market (-20%) for market risk, or living beyond 80 as a longevity risk. It doesn’t take the risk to the end point of actually running yourself into bankruptcy. It’s just looking at the likelihood of a material risk in each area, which might result in you having to adjust your retirement plan in a significant way.

LikeLike

Got it. Thanks. I agree. The chances of living past 80 are probably higher than a massive, sustained, market loss.

LikeLike

Chief, I recently posted a comment on another finance website article about people not have saved enough to retire. I posted about the virtues of FIRE and pointed out that the funds you invest when you are young will someday be the majority of retirement funds due to the magic of compounding. My post also suggested that it takes around 25 years to achieve FIRE.

I received some negative comments from another commenter with the handle “Ol Lady” which harped about missing out on opportunities for fun when you are young. Her final comment was she wished she could be my heir.

My family is not very much worried about the risks you listed because we have planned well. “Ol Lady” will someday start worrying about the risks, but by then it will be too late.

LikeLiked by 1 person

Funny that ‘OI Lady’ can’t think of a plethora of opportunities to have fun without spending a lot of money! That wasn’t a problem for me at all. 🙂

LikeLiked by 1 person

I think your website and all the adventures you describe proves that point.

LikeLiked by 1 person

I just read that brief. My observation of young people (below age 45) who tout FIRE, is that they market FIRE like people market high intensity workouts, fancy cars, expensive vacations and other lifestyle aspirations. The selling of things one aspires to achieve.

I like to think that my father, six years gone was FIRE when it wasn’t cool. He and my late mother always lived below their means and built their house, with cash in 1960. They added a garage in 1962, and I recall in 1967? When they finished off my sisters room, prior to that we could not open the door as the floor was only floor joists and between was the backside of the kitchen ceiling!

We are having the estate planning discussion with our adult children this week. We also have lived below our means and in retirement three years now, have not and have no plans or need to draw from IRA type investments until RMD at 72, or our nest egg investments. Yes, I have a pension and wife draws social security (waited until full retirement age). I also earn about $30K annually consulting which is fun. I also probably do consulting worth $20K if billed which mainly consists of drafting and giving presentations and mentoring which I find enjoyable and it keeps me sharp.

I have inherited Chronic Kidney Disease which may, or may not impact my longevity. Health risk is what impacts my wife and I more than any other risk. We view the nest egg and condominium (paid for) as our method to fund skilled nursing if needed.

YOLO, and FOMO cause many to miss life’s joys. Many in society suffer from the grass is greener syndrome. Influencers lead people to a mindset of scarcity rather than an appreciation of abundance that most in North America have, or have the ability and opportunity to achieve.

LikeLiked by 1 person

I agree that something doesn’t quite smell right, when it comes to young FIRE influencers. Like all influencers, most of them seem to be selling something – pdf books, financial counseling, or at least advertising.

That’s not all of them, of course, but many of them, for sure.

They seem to spend so much time working in their look and hype, I wonder if it has become their full time job?!

LikeLike