I spent the evening of New Year’s Day (observed) tallying up the ugliness of our 2022 year-end financial performance.

The returns weren’t great. Not at all. It looks like our retirement savings took a huge dive. Our retirement nest egg fell a whopping -16.9%. That’s much worse than I had imagined.

Our losses were all centered in the plunge in our equities. The S&P 500 was down a staggering -19.4%, driven by fallout in tech stocks. You can see from the chart below that the huge declines this year basically wiped out gains from the two previous years – which were very strong – making the 3-year return roughly flat (+1.1%/year).

That said, as you look at the bars on the chart from left-to-right, you quickly see that not all has been lost. The 5-year annualized return rate is a solid +7.9%. Since I ‘FIRE’d’ back in 2016, we’ve seen 11.1% growth. That’s above the 10-year number and well above the span of my professional career back to 1989.

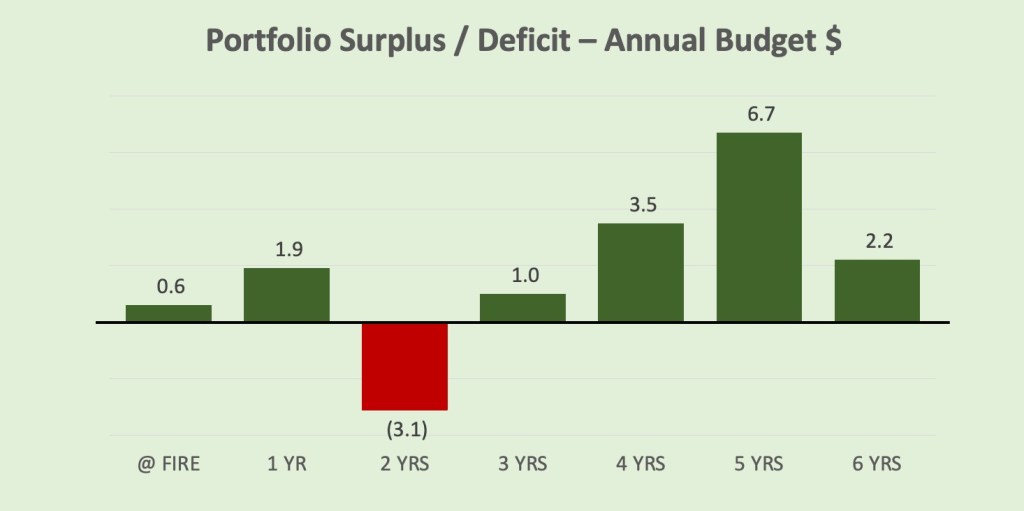

As a result, our portfolio is sitting in a good place, if not as great as it was last year. Measured in terms of an annualized budget surplus, we are running 2.2 years ahead after 6 years of early retirement. That’s a good cushion.

I still wish global governments hadn’t pursued their costly & disruptive pandemic response plans. They have had such a negative impact on debt, inflation, interest rates, and corporate earnings – and did little to slow the CV19 virus. Still, I hope it’s finally time to move forward to brighter horizons in 2023.

H A P P Y N E W Y E A R 2 0 2 3

Image Credit: Pixabay

“’Tis the song, the sigh of the weary,

Hard Times, hard times, come again no more.

Many days you have lingered around my cabin door;

Oh! Hard times come again no more”

— Stephen Foster, 1854

LikeLike

My cabin door is looking pretty beat up. I hope things swing to the good in 2023. The last ‘good’ year I can remember was 2019. That year ended with my heart attack!

LikeLike

Last year was a fearful market. Fear drives down market prices, but lower market prices means current yields go up for dividend investors. My market cap was down approximately 4% after taking out 2.5% to live on. The combination of reinvesting around 40% of my dividend income, opportunistic trading, and dividend increases increased my annual income by slightly over 18%.

I am following closely The Freedom Caucus’ efforts to end business-as-usual in Washington D.C. I like fellow Badger Jim Jordon’s planned changes for the Federal Government and hope he prevails. That will help set us up for a better 2023 by ending governmental craziness.

LikeLike

Well, now is the time for them to drive for change. The House of Representatives seems to have become a private fiefdom of whoever is the current House Speaker. Now is the time to return more power to individual members to introduce bills, debate & amend.

LikeLiked by 1 person

Sounds like a plan to me. The founders of our country did not want a monarchy or overly centralized power.

LikeLiked by 1 person

I’ve mentioned it before, but we have always looked at our investments from two competing angles (Traditional Equity/Bond assets verses Rental Real Estate assets) . Our traditional retirement funds remain untapped after 5.5 years of early retirement (still won’t tap these for at least two more years). These are essentially our traditional equity/bond index funds. Our overall equity/bond portfolio was down a total of 16.1% for 2022. Ouch! The equity/bond diversification did NOT do its job in 2022 as bonds were down approximately 14% for 2022, so they did not offset equity losses as one would typically like to expect they would react. However, our second major category of investments (rental real estate) assets nicely countered those losses with a 23.2% asset gain in value in 2022 primarily due to rent inflation, which drives asset appreciation. The rental investments also netted a 7.2% cash-on-cash ROI, which would have been closer to 12%, but we did several necessary capital improvements on buildings late in the year that drove the overall ROI down to 7.2%. (These were also strategic CAPEX spends during a good year to help manage our income levels to maintain ACA subsidies.)

Interestingly, our overall net worth was up ever so slightly overall (approximately $12k) for 2022 thanks to the major offsetting investment classes. These were huge asset class swings to net a tiny $12k gain for the year, but I’ll take it given the crazy financial year we’ve all experienced. (I laughed to my wife that I haven’t been this excited about a $12k annual net worth gain since our twenties!)

LikeLiked by 1 person

I find it interesting that an owner of capital takes pride in eating at the trough of government welfare. I’m speaking of the ACA subsidy, Obamacare! Comments on the same post about both the Freedom Caucus and Obamacare and both posts are seemingly for both.

A fiscal conservative used to be proud to be self-sufficient AND against those who take advantage of welfare programs. Being proud to keep income levels low to take advantage of someone else’s taxes supporting your health costs does seem a bit hypocritical and historically un-American

LikeLike

Dave,

Lol! I absolutely love comments that have little substance and even less intelligence!

So I’m certain you don’t file your returns utilizing any IRS provided deductions, tax credits or other legal tax breaks provided within the IRS tax code. Right?…Because that too would be considered by many as taking free government monies from other’s tax payments. I’m sure you’ve also always told the IRS to just keep your over payments and even sent your refund checks back to the IRS. Right? I’m sure you always pay extra taxes above and beyond your normally required tax level. Right? Yeah…I didn’t think so, because you are (inaccurately) viewing those tax deductions, credits, and tax breaks differently. Primarily because it’s only fair you’re the one gaining and if someone else is paying… Right?

Before you embarrass yourself further, take a look in the mirror and take measure.

I can assure you that I’ve paid many more taxes during my lifetime than any twenty (or more) average combined citizens. I also guarantee that I have provided more jobs and incomes to individuals and families during my lifetime (and through businesses that I’ve owned or own) than any other average one hundred (or more) citizens combined. I also continue to employee more people in retirement than any other average twenty (or more) citizens combined provide, which provides (way) more taxes and support to our economy than most citizens will ever hope to contribute. So do I take a legally provided IRS tax break? You bet your sweet @ss I do! Just like you and every other citizen that files a tax return! So before you chime in with an embarrassing comment on a social media platform, that you clearly don’t fully grasp, I suggest you know your topic and your audience a little better. Don’t EVER call me un-American…I’ve more than paid my dues in many ways to my country. You do NOT know me.

So enjoy your day Dave, and thanks for the comment! It gave me a good laugh today and reminded me just how inept our education system has actually become. 😉😆

LikeLike

Actually I admit that my household is a recipient of welfare as my wife receives Medicare and Social Security, I’m not there yet.

I do take the tax breaks allowed although there are not many and I just mailed my quarterly tax payments to the IRS and Franchise Tax Board.

I did not call you Un-American, I simply pointed out that historically welfare type benefits which Obamacare is has been an Un-American view contrary to self sufficiency.

Don’t act like such a sensitive snowflake. Note that I didn’t call you. Snowflake!

LikeLike

Dave,

Thank you for proving my point on every level. Out of respect for the owner and other readers of this blog, I’m going to let this go without further comment. I hope you have a wonderful day.

LikeLiked by 1 person