The new “Trump Accounts” 530A program is now officially rolling out, and millions are taking notice. The app is suddenly the top download on the Apple & Google app stores – again proving the popularity of “free” government money from politicians in an election year.

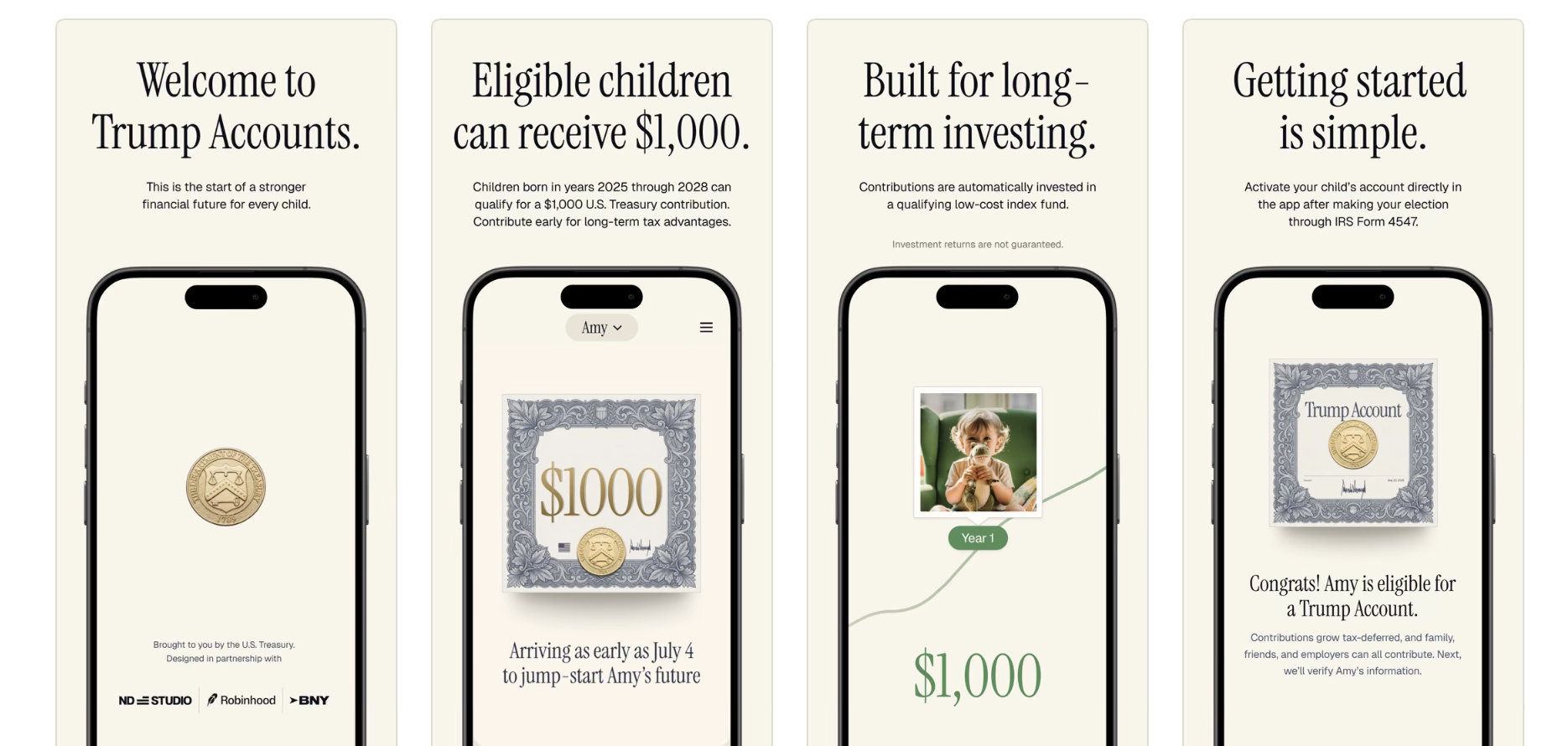

At its core, the program is simple. Children born between 1/1/25, and 12/31/2028, are eligible to receive a $1,000 contribution from the federal government into a tax-advantaged investment account. The account is held in the child’s name, while a parent or guardian serves as custodian until age 18.

Where does the money come from? Ultimately, taxpayers. The $1,000 seed deposit is funded through the U.S. Treasury. Additional contributions can come from parents, grandparents, employers, charities, and others, subject to an annual limit of $5K.

- Once the beneficiary is 18, funds can be withdrawn for certain qualified purposes, such as:

- Higher education expenses

- Starting or buying a business

- Purchasing a first home

- Other specified uses under the law

The tax treatment depends on how the money is used. Qualified withdrawals receive more favorable tax treatment, while non-qualified withdrawals may be subject to ordinary income tax and potentially additional penalties.

As a taxpayer – and supporter of government fiscal (and individual) responsibility – I have mixed feelings about this program, but likely would not have approved it if I was “King for a Day”.

On one hand, I like the idea of encouraging investing, ownership, and long-term wealth building. A child who receives $1,000 at birth – and adds to it consistently – could have a meaningful financial head start. Anything that gets young Americans thinking about investing instead of consuming has some merit.

On the other hand, let’s be honest about what this is. It is another government wealth-transfer program funded by taxpayers. At a time when the federal government is running massive deficits, carrying a national debt measured in the tens of trillions, and unable to rein in spending in the most modest of ways, it seems fair to question whether Washington should be creating yet another benefit program.

Politicians in both parties have become remarkably comfortable handing out money. Republicans call it one thing. Democrats call it another. The bill still arrives at the same mailbox. I think in short time, this program will expand and become one of the biggest income redistribution schemes developed by government since ObamaCare.

Besides, I’m not convinced a program was really necessary for most Americans. There was nothing stopping parents, grandparents, and others from already “gifting” children up to $18K a year. Put into a an HSA, Roth IRA, or 529 Education Plan already carried meaningful tax benefits.

That said, I know we also live in the world as it exists, not the world we wish existed. If your child qualifies, my recommendation is straightforward: absolutely take advantage of the program.

You didn’t create the rules. You didn’t vote for the deficits. But if the government is offering your child a $1,000 investment account, there is little benefit in standing on principle while everyone else participates.

As I’ve often said about tax credits, rebates, and government incentives, “if they are dumb enough to give out money, you should be smart enough to take it.” Who knows? If invested wisely and allowed to compound for decades, that $1,000 might help your child reach financial independence a little earlier than they otherwise would have.

What are your thoughts on this new program? Do you know people who will be able to take advantage of it?

Image: Apple App Store