Now that I am retired early and enjoying my first month without work, people are asking me for advice on how much THEY need to save to retire themselves. Many people don’t seem to know where exactly to start. Calculating the money needed for retirement feels like walking into a foreign casino to them – full of opportunity, but also fraught with risk.

With that in mind, I thought I would share the two SIMPLE “lenses” or tools that will help you understand what you might need. It will give you a decent sense of where you are at and won’t take you more than 10 minutes to use.

- 4% rule – Based on what is known as the Trinity Study, the 4% rule is the concept that in a typical 30-year retirement, one could withdraw 4% of retirement savings annually and be highly unlikely to risk running out of money. The 4% rule is a great starting point early in your planning – because it is such an EASY concept to apply. Just consider what lifestyle you want to have in retirement (spending) and multiply it by 25. If you want to retire early, or be more conservative, use a factor of 33 (3% withdraw rate).

- FIRECALC – This online calculator (firecalc.com) takes the root math behind the Trinity Study and lets you play with the details. It a simple and easy to use Monte Carlo analysis that utilizes historical investment returns back to 1871 to understand the probability behind your investment returns. History is, of course, no guarantee of future performance, but it is a good place to start with two World Wars, the Great Depression (and Recession), and periods of irrational exuberance included in the data set.

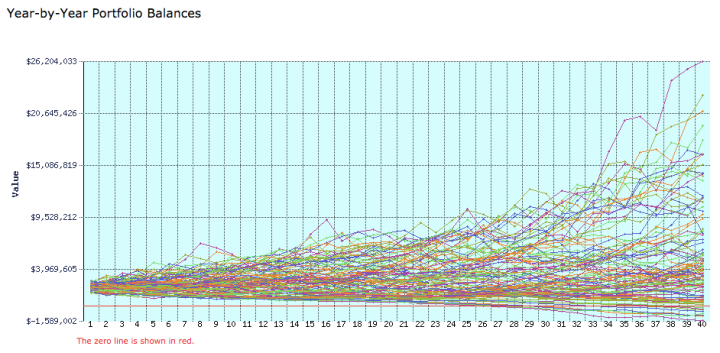

You simply input three key factors: 1) retirement spending; 2) retirement nest egg; and, 3) spending horizon (ie 30, 40 years). It then kicks out a graph that shows you how you would have faired for retirements starting each year over the last 100+ years. In this example, I’ve used a $1.5M nest egg with $60K in spending over 40 years: It shows that 85% of the lines stay above zero – meaning you don’t run out of money:

Notice that under the best of historical circumstances, the $1.5M nest egg grows to over $10M. The worst line leaves you almost -$1.7M in the hole. Obviously, budgeting in retirement is an ACTIVE process – we all need to adjust to actual market circumstances. Note that it also 20+ years until the best & worst possibilities start to really emerge. The fact is, the longer we live, the more likely we are to run into extreme bull or bear markets that leave us in the penthouse or the basement.

Additionally, FIRECALC is a terrific tool because it allows you to play with assumptions in a lot of different ways. Beyond the basic 3 inputs, there are tabs that you can use to add in your Social Security, your pension, different investment assumptions, and different spending philosophies. All of which are reflected in historical returns of those choices.

What is the right level of confidence or probability of success? That really depends on you. Because the tool his face is historical return, it can only be one lens on your decision know when to retire. For us, we look for a number of 90% or greater. Others, feel comfortable an 80% probability.

I really wanted to feature FIREcalc in this post, because it not only helps you get a sense of where you are at, but also allows you to LEARN what works best in planning your retirement.

To show my support for the tool and encourage others to use it (it is a user-supported, wiki-site), I will donate $2 for every MrFireStation.com visitor who comments to this post about their experience using it (for the good or bad), up to $100 dollars over the next week. 🙂 Should be fun to see …

Image Credit: Pixabay

- BTW: The 4% Rule and factor of 25 is fun to apply to fantastic “What If’s” too. A friend dreamed, wouldn’t it be GREAT to have enough money to live at the Ritz Hotel in Paris full time? Well, assuming that’s about $1K a night = $365K a year x 25 factor = $9.1M nest egg would be needed to achieve that dream.

UPDATE (5/18/16): I received 17 comments to this post and donated $35 to FIREcalc via PayPal today. Thanks to everyone that tried out FIREcalc – everyone said it was a valuable tool!

i stumbled upon firecalc about 8 years ago. it was a huge help during the great recession to see lots of what ifs. take the time to look at the options available, its extremely flexible in planning both sides of income and expense to simulate results. just remember mr firestation that 90% success for those glass half empty guys means 1 in 10 fail, far to high a failure rate for me ……

LikeLiked by 1 person

Everyone has their own comfort level certainly – ours is 90%, although that assumes we have some luxuries in retirement we didn’t have while I was working. Thanks for the comment!

LikeLike

I loved this tool! Thanks for sharing and making a donation. win/win. It is such a good reminder to have a longer horizon than the crazy/frequent market ups and down. It affirmed my decision to retire early as well. Keep the hubby working a bit in a job he loves and both be done in 5 years. 🙂

LikeLiked by 1 person

It is a terrific tool – I could play with the variables all day long. It’s fun to look at different options.

LikeLike

This was fun! Another affirmation that DH and I can retire early in just 37 months 🙂

LikeLiked by 1 person

Just 37 months? – That time well fly, I’m sure!

LikeLike

That’s awesome. I’m 41 months away myself thanks to FireCALC :). I thought I was 10 years away, but that tool’s flexibility allowed me to see the bigger picture. It’s amazing.

LikeLiked by 1 person

Wow – that is a huge finding for you, isn’t it? Glad the tool allowed you to look at things in a new way!

LikeLike

Great post. I’m definitely familiar with the 4% Rule but that is the first I’ve heard of firecalc.com. Thanks for the info, I look forward to playing around with it under different scenarios!

The Green Swan

LikeLiked by 1 person

It is good fun to try different scenarios. There are a couple other monte Carlo calculators for retirement that you will find online – each one has some unique twist.

LikeLike

I’ve used firecalc before, and have also used cfiresim. I like both tools. Today I went back and played with firecalc – good fun! I’m somewhere in the range of 70% – 100% there, depending upon how I play with the numbers, and how I see “early retirement” playing out for me. Very cool!

LikeLiked by 1 person

It sounds like you are right on the button for where you want to be. Now you can think about safety margin and luxuries in early retirement. Thanks for the comment!

LikeLike

It’s been awhile since I last visited FIRECalc, so I revisited today. Thanks for the reminder! Entering my current spending, nest egg, and a 60 year time horizon to 100 gives me an 87% chance of success. Adding an estimate for social security for the wife and I boosts it to 99%. I like those odds, but when I project the nest egg from 5 more years of work, I’m up to 100%!

Oh, and thanks for sending them some $. Here’s hoping we see 46 more comments and you’re out $100. 😉

LikeLiked by 2 people

Wow – a 60 year time horizon! That is some window to plan for, but it sounds like you are right where you need to be. Especially if you work another five years. I thought the donation angle would be fun – a lot of comments rolled in today while I was out golfing.

LikeLike

My Grandmother made it to 99, so I might as well plan for 100. Time will tell!

LikeLiked by 1 person

Oh I’ve spent way more hours than I’d like to admit messing with FIRECalc and cFIREsim (http://www.cfiresim.com/) over the past year than I care to admit. 🙂

LikeLiked by 1 person

Yes, I’ve played a bit with cFIREsim too. I think it is a bit more sophisticated – certainly be interface is better – but I worry about being too exact with what should be a rough estimate. Thanks for the comment, Maggie!

LikeLiked by 1 person

Thanks, MFS! What the FIRECalc site did for me is allow me to breathe a little easier, as I plugged in the numbers we know right now…I’m fairly certain we’re going to be OK. It also made me dream a little – not that I’m planning on living at the Ritz any time soon, but a few more cruises in there would be nice!

LikeLiked by 1 person

We did put in a higher spending level then we have been living on for our early retirement plans. A big part of that is increased travel. It’s fun to be able to play around with the numbers and see how it affects the Monte Carlo analysis. Thanks for the comment!

LikeLiked by 1 person

Awesome post. I have been using FIREcalc for years. Both before and after my retirement. I also recommend its use to anyone serious about retirement and gauging their plan vs savings. Cool that you are donating your money and spreading the good word. For all the times I have used them I owe them another donation myself.

LikeLiked by 1 person

I admit that we have not donated to them before. I have used it for about two years, and thought that it gave me a lot of value that I would share it with others. You are the ninth commenter so far today!

LikeLike

I used firecalc before. Fun to run the varies scenarios to see the possibilities.

LikeLiked by 1 person

Thanks, Brian – you are commenter number 10!

LikeLike

I did use FireCalc and was impressed that I could vary the scenarios. I used a 50/50 stock / bond split, a 4% withdrawal rate and a 35 year term. Came up with a 94% probability.

Keep in mind their standard asset allocation is 75 / 25 stock / bond which seems to a bit too aggressive for me. Any other thoughts on the optimal asset allocation that allows one to sleep at night?

LikeLiked by 1 person

Yes, I agree that the base portfolio allocation split is a bit aggressive. We have had a 50/50 split in the past, but last summer my financial advisor suggested we move it closer to a 60/40 split as we have a pretty long retirement horizon. Thanks for the comment!

LikeLike

I’ve used it too, and loved it. You can also use it during the building phase, as there’s a tab where you can feed in in what year you’d like to retire* and how much you’ll save every year until then.

I think the best thing to use it for is for estimations – of course things will never turn out exactly as planned.

*Maybe it could use another option where you can feed in: “I’ll work until I have $xxx,xxx ; so that it varies your retirement date with the different returns of the market.

LikeLiked by 1 person

I didn’t know it had that capability. That’s useful – to estimate your savings by year AND what your ultimate number should be, based on historical performance. Thanks for the comment!

LikeLike

I use FireCalc a great deal and find it very useful. Where most of our investments are held in Vanguard index funds, we do rely on Vanguard’s longevity calculator to make sure we are still on track.

Happy to hear that you’re enjoying your retirement!

LikeLiked by 1 person

Thanks – I have not seen the Vanguard longevity calculator. I will have to check that out – thanks for the tip!

LikeLiked by 1 person

I’ve never used this. Like Lynn at Encore Voyage, running this actually gave me a deep breath of relief! I had 100% (!) based on our current retirement savings portfolio, 30 year projection and a reality one-year in-retirement budget (which was actually higher than I anticipated). So, no plans on living at the Ritz, but feeling OK about planning those dream trips. All that savings for years has paid off.

LikeLiked by 1 person

Good to hear! It’s a fun tool to play around with – if you are at 100%, you might choose to eek out a little more spending.

LikeLike

FIREcalc and CFireSim are fantastic tools — so much more robust than the 4% rule alone. I’ve also found it helpful that I can include other sources of passive income as monthly cash flow in the projections.

LikeLiked by 1 person

Thanks, Matt – 4% is a good place to start, but FIREcalc & CFireSim really dimensionalize the risk we might face.

LikeLike

Thanks for sharing these details especially the FIRECalc… I am new to your blog and so far am really enjoying living vicariously through your posts!

LikeLiked by 1 person

Thanks & welcome to the Fire Station – I’m in week3 of my early retirement …

LikeLike