We had a nice sit down with our financial planner last week for our ‘annual check-up’. As you can imagine, the update was very good given how well the markets have been doing, despite the pandemic.

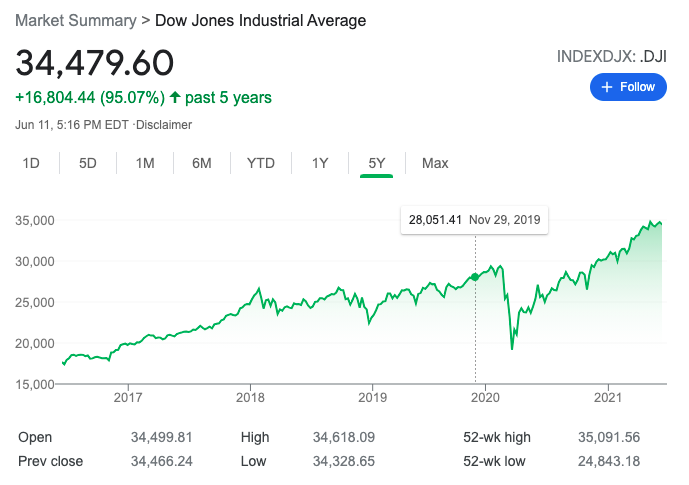

I honestly believe that I couldn’t have been luckier to pull the trigger on retirement 5 years ago. Since then, the stock market has been on a tear, growing 95% overall, or +18.1% annually. They say that the sequence of your returns are very important in retirement and we’ve started out with a very strong streak.

Here’s the DJIA since 2016 – starting at 18K and now over 34K …

As a result, our planner felt very good about our outlook, even with our expensive new goal of a second home/villa/condo in Florida to winter in. We still have a lot of planning to do on our Florida Project, but the bull market over the last 5 years has allowed us to afford a much better early retirement than we were expecting financially.

Here are couple other interesting observations …

- He’s not too concerned about inflation. “We haven’t had runaway inflation in 40 years”. The Fed’s description of inflation as “transitory” seemed plausible.

- They are using a 2.5% long-term inflation assumption. Their economists feel the Fed has a good handle on how to manage inflation.

- At age 55, our portfolio mix of 70% equities and 30% cash/bonds/fixed notes seems about right. We also have some added security in my MegaCorp pensions.

- The stock market feels more tipped to risk than upside right now, given the Schiller PE index, but corporate profits are hugely uncertain coming out of CV19.

- The benefit of deferring my large pension has changed quite a bit from 8 years ago when I left MegaCorp. He’s now recommending taking it all now, as the value only goes up about 10% by delaying 10 years. Might as well start cashing in.

- We are carrying 2-3 years spending in cash – that continues to feel like a good cushion in the event of a market downturn.

All in all – as I used to say when I was working – “good numbers make good meetings”. How are you feeling about your portfolio and spending in retirement? Are you able to ramp up your lifestyle given the strong bull market over the last 5 years?

Image Credit: Pixabay

Good numbers make good meetings, love it 😀 Thanks for sharing, and glad to know that you’re on a good track!

LikeLiked by 1 person

We’re in year 4 (for me) and year 5 (for my wife of early retirement, and likewise, we are up significantly over the past 4-5 years. We are living solely on our rental property income so far, and have not even begun drawing down any of our 401k’s or IRA’s. So our ramp up will still begin at age 59.5 years old as planned, but it could effectively be substantially larger than originally expected.

LikeLiked by 1 person

Great to hear! Are you thinking about any lifestyle upgrades that weren’t in the original budget?

LikeLike