Prices are going up. Consumer price inflation ballooned to 6.8% in November as massive increases in government debt and supply-chain issues over the last year were reflected. The Fed & Biden believe they can get back to a 2% annual average target, but clearly that’s going to take some doing.

Retirement plans are especially susceptible to rising prices as fixed investments, pensions, bonds, and social security don’t always keep up with inflation. When I retired almost ) years ago, I put in a 2.3% assumption, based on the long-term Fed Target of 2.3% and a JP Morgan report that I read.

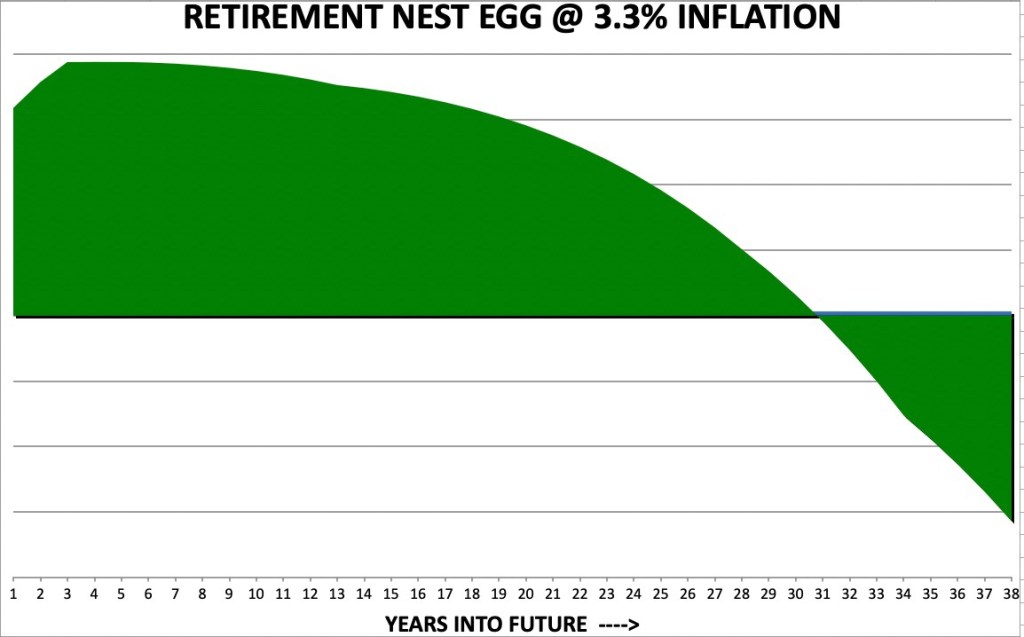

I knew then that our inflation assumption has a huge impact on how long our nest egg lasts. With Friday’s inflation news, I decided I would model out a 1 percentage point inflation change to see just how ugly it looks.

Here’s the baseline scenario 2.3% …

Here’s the same portfolio at 3.3% …

Isn’t it shocking to see how different they are? A single percentage point doesn’t seem like a lot, but compounded year-after-year it makes a massive difference.

Now the hope is that most of our investments maintain their real rate of return above the rising rate of inflation. We have 5.0% capital gains and 2.5% dividend growth estimate built in our model for a 7.5% total annual return. If inflation is 1 point higher, we need our investments to be 8.5% going forward. I think some of our investments will keep up, but others won’t.

How much inflation risk is in your retirement plan?

Image Credit: Pixabay

As this moment I think the impact of inflation on my retirement is pretty limited. While I’m definitely seeing higher gas and food prices, those are not a huge part of my regular spending. Other costs like insurance, gas / electric, electronic services (ie cable / phone / Netflix /etc) are about the same. We also own our house outright with no mortgage, so the impact of higher rents don’t really impact us. Even if we sell our house and move, I expect that the higher house prices we’ll see will be offset by the higher value of our current home.

LikeLiked by 1 person

Agree – we are in about the same situation. I didn’t buy a new vehicle this year, so I paid a definite premium for that. The Jeep was definitely a purely discretionary purchase though.

LikeLike

Average inflation over past 30 years was 3.5% per year. So I assume that. A massive outlier like this year makes me question whether I can assume that going forward. Hopefully, we will return to mean sooner rather than later. Protracted bad decisions being made by proactive centralized government cause much uncertainty because normal market conditions and operations are distorted by unintended consequences.

LikeLiked by 2 people

We will be returning to the mean and I expect it will happen right after the 2022 midterm elections. The current inflation differs from the inflation we experienced during the 70s because today’s is caused by bad government policies that can be undone. The USA did not have the ability to become oil independent during the 70s oil shocks based on a change in government policy. The free market did this by working to innovate in the energy field at an unprecedented rate.

From what I am reading and seeing in my news sources, the Omnicron variant is much weaker and more contagious, so people are going to start building immunity whether they are vaccinated or not. Covid is going to start sputtering out, which will reduce government’s reasons for having an excuse for having do much unwanted control over ours and the market’s freedom.

The timing is right for a new Contract with America to provide President Brandon with much needed adult supervision.

LikeLiked by 2 people

GOP’s ‘Contract with America’ was one of the best branding jobs ever done for a Congressional campaign year.

LikeLiked by 1 person

I think the average is actually quite a bit lower than that, Bowmanifesto. I’m seeing a 30 year average closer to 2%-2.5%. I guess you can start spending frivolously now! 😉

https://tradingeconomics.com/united-states/inflation-cpi

LikeLiked by 1 person

“During the observation period from 1979 to 2020, the average inflation rate was 3.5% per year.” Source: https://www.worlddata.info/america/usa/inflation-rates.php

Either way, 2021 inflation was heinous and avoidable. Let’s not repeat the avoidable!

LikeLiked by 2 people

Yeah – 1979 is 42 years ago. That extra 12 years picks up the horrible early 1980s inflation. Let’s hope we aren’t replaying that right now!

LikeLiked by 1 person

My wife and I could be receiving Social Security now at almost the maximum rate, but we are both waiting until we are 70. By waiting the payout grows 8% per year plus the COLA. So for this year the return on waiting is almost 14%. We are also mostly taking nothing out of our IRAs and letting the dividends reinvest and grow.

We have 4% divided grow rate baked into the plan and currently are letting the 4.6% yield reinvest. Capital gains are nice, but we are not planning on them as a part of our income strategy, because you don’t know whether Mr. Market will be in his manic or depressive phase

LikeLiked by 1 person

Waiting to take SSI – as long as you are reasonably healthy – is about the best return you are going to get at a low level of risk.

LikeLiked by 1 person

I never want to touch my principal AKA live on capital gains and prefer to live on a growing income stream based on dividends.

When Mr. Market is in a state of depression, he is willing to pay less for stocks so you will get a higher current yield on your investments. Reinvesting dividends at a higher current yield that is growing, will grow your cash income faster.

When Mr. Market is in his manic state, he is willing to pay more for stocks so your yield will go down. This is when you look for opportunities to sell your over priced stock to Mr. Market and trade into another with a higher current yield. I especially do trades to upgrade my dividend income stream in IRA accounts where I don’t have to pay taxes on the transaction.

Of course you always want to get out of Blockbuster type stocks after you see that NetFlix has destroyed their business model.

LikeLiked by 1 person

Wait what? I should get rid of my Blockbuster card? 😉

LikeLiked by 1 person

Inflation isn’t the impact to our lives as much as the decrease in services available. Restaurants that don’t open until 5:00 which we used to eat at in the afternoon. Fewer Uber rides available so we spend the night at an airport hotel before flights.

Congress at the moment seems to be working as designed. People want the infrastructure bill to pass. What they don’t want is the government calling support for child care “infrastructure”. We provide a lot of support for families but society doesn’t want to pay additional for child care.

LikeLiked by 1 person

Government support programs for childcare will create a false economy similar to what we already have in higher education. In the mid to late 70s most students at public universities paid their own way by working long hours at entry level jobs during the summer months and graduated debt free. Then along came government help in the form of student loans and higher education has risen for the last four decades 50% faster than inflation and entry level job salaries. We could break the back of higher education inflation by outlawing student loans.

“The nine most terrifying words in the English language are I’m from the government and I’m here to help.” – President Ronald Reagan

LikeLiked by 1 person

Truth!

LikeLiked by 1 person

I’m wondering how long it’s going to take for front line jobs to get filled post-CV19? We live close to the largest shopping mall in the entire USA – the Mall of America – and it didn’t open until 11 AM last Saturday, which should’ve been the biggest day of the year for retailers.

LikeLiked by 1 person

I have been to Mall of America when visiting my wife’s relatives, so am aware of the scale. The last two decades have not been kind to US workers due to offshoring, outsourcing and illegal labor. Entry level jobs have not kept up with inflation as evidenced by them not paying for public university like it could when I went. This is the time for labor to make up for some lost ground.

I also suspect the Mall of America was running into trouble before Covid hit. They are probably repurposing away from retail of anything that you can buy online to activities that people want to do in person.

LikeLiked by 1 person

The Mall of America was doing well pre-CV19. They had just added a big retail/restaurant expansion, a second luxe hotel, and an office building. They had a big attached $350m indoor water park planned, but the pandemic ended that. They’ve always been a mall that mixes shopping with a big dose of restaurants & entertainment. As you say, that seems to be the right formula going forward.

LikeLiked by 1 person

When I built our initial long term spreadsheet six years ago, I built in 3.1% average inflation factor for expenses because that was the overall long term average of the US market from 1913 up to that point. We’ve been in a very unusual low period for the last 20-30 years. 1990-2000 avg =3.08%, 2000-2010 avg =2.54% and 2010-2019 avg =1.75%, 2020 avg =1.78%. So our new higher inflation is a shock to most short term investors. Even during my investment lifetime (since about 1987) we’ve been very fortunate from an overall inflationary standpoint. You are correct, that even small changes compound the impact over long retirement periods. It was the biggest killer of retirement plans in my early research. We also built in very conservative returns for our investments, so we’ve been overachieving on both fronts for our first five years in retirement thanks to the stock market side of our portfolio. Sooner or later I knew we’d have hits though…

We’ve been fortunate to this point. Inflation was a big reason I focused a large portion of our portfolio on rental property investments. Rents tend to keep up with inflation. We actually just issued the largest increase in rental rates since I started our rental investment business just over 12 years ago, that will take affect in January 2022. This will increase our gross receipts on our 54 properties by approximately 16% and better align our properties with our particular rental markets. (It also corrects some overdue increases in our case.) I also modeled our rental property inflation growth very conservative (in our retirement model) six years ago at 1% rent growth. But with this new increase, we will realign our rental receipts with actual inflation (ie. we are getting better investment returns than we modeled six years ago as a result). The net effect, we are ahead of our models to date. The new higher inflation may correct our over achievements to date. I’m still comfortable with our model at 3.1% inflation factor and hoping it levels back out from the recent 6.8% factor.

LikeLiked by 1 person

Wow – a +16% price increase. What has the reaction been among your tenants? I guess if that adequately aligns you with the market, they will see that, but I’m guessing that required you providing some comparisons.

LikeLiked by 1 person

Tenants were given 3 month written notifications. And yes, we were aligning with some extraordinary rental increases that have been occurring in our markets over the past year and a half. I believe the COVID related rental eviction moratorium caused some unintended reactions in many markets, resulting in significant rent increases as the moratorium lifted. Typical governmental intervention at its finest! Plus, we had some units that were already a little low to begin with, so somewhat correction related. I suspect there will continue to upward movement in rents, if inflation continues to expand in 2022. We shall see.

It has proven to be a decent inflation hedge for our portfolio over the years. Real estate doing what it does best. Slow and steady…

LikeLiked by 1 person

Nice! After the CV19 challenges of being a landlord, now you are getting ‘paid back’.

LikeLike

I first went to Mall of America when they had an indoor amusement park run by Cedar Fair with a Peanuts theme. This was a company that I had invested in for long time and their distributions paid one of my son’s way through college. My investment thesis was developed while working a summer job in the Dells and the President told me regional parks do well when the economy is down because people who normally go places like Hawaii downscale and go to the Dells. When times are good, people who cannot normally afford to go anywhere can go on vacation to the Dells. This worked great until Covid hit and they suspended their distribution. The business in the Dells was very well managed, but they just shut down operations after being in business 75 years due to Covid closures.

I had two investments that cut their dividends; Disney and Cedar Fair. I feel like researching if Disney’s CEO has paid himself a bonus, while he has given us retirees nothing, and asking him why he isn’t sharing our pain at the next annual meeting?

LikeLiked by 1 person

Yeah – Cedar Fair also owns our Valley Fair theme park. Triple Five – which owns MOA – now operates the MOS theme park directly. It has a Nickelodeon theme now, not Peanuts.

LikeLiked by 1 person

Chief, A couple questions about Mall of America’s change in strategy. The luxury hotel and waterpark make sense as a way to give respite to people in the middle of the winter. Edmonton’s Mall which is the biggest in North America has had this for decades in a location where the weather makes the Twin Cities look like the banana belt in comparison. Restaurants I get. You mentioned new Retail. Curious to find out what the new retail establishments are and what they offer? Must be something unique?

LikeLiked by 1 person

Temperatures in Minneapolis & Calgary are closer than you think. It gets quite a bit warmer here in the summer, but only about 5-degrees (F) different on average in the Winter. We get hit with ‘Alberta Clippers’ constantly. Both malls were built by the same developers.

The new North Wing at MOA has a 2-story Zara on one side and a 2-story H&M on the other. Not exactly unique. There is also a third floor food court with about 15 places and at least 2 ‘nice’ restaurants. Also, a new rotunda, two event centers, a JW Marriott, and an office building. Smaller stores are intended to fill up the retail on the wing, but everything screeched to a halt with CV19. The original idea was to bring in LV, Tiffany, Gucci, and other luxe brands. Most of those are also at the nearby Galleria, which has had a corner on luxury stores for decades in the Twin Cities.

The new water park was going to be quite a boondoggle (and maybe still will be). The city was going to build it on MOA land, gift it to a non-profit (so MOA wouldn’t pay taxes), pay MOA rent for the land, and assume all the risk of running it! MOA gets a giant new amenity at no risk to themselves that then pays them money! Crazy misuse of government power in my opinion. Did I mention there is already a large, privately-run, hotel/water park across the highway? Feel bad for those investors.

LikeLiked by 1 person

Many the local government is concerned about having an Albatross on their hands?

In the time I have lived in LA, I have watched the city chase many large, well paying business out of downtown including ARCO, large banks, etc. because they started collecting a gross receipts tax that caused the business to move out of town to avoid. Then after having a policy that decimated the downtown, they offered incentives for developers to come in and fix the blight by building Staples Center. Unless your name is Labron James, you probably made more money working at ARCO than a Staples working part time vending beer, which had the highest number of jobs paying over $100,000, when they moved to Sacramento.

Bad government policy trying to correct the last set of bad governments policies. Or, a boondoggle for the politically connected perhaps?

LikeLiked by 1 person

Here’s the write up on the MOA water park … https://www.bloomingtonmn.gov/port/news/quick-facts-about-water-park-project-2021-02-01

LikeLiked by 1 person