When I first started working in the late 1980s/early 1990s, we would keep our meager savings at the MegaCorp Employee Credit Union. I would walk down to the lobby of our 40-story tower almost weekly to make a deposit, transfer some money, or buy a CD.

Buying & cashing Certificates of Deposit is something it seemed like we did all of the time back then. Interest rates were good and we had a whole “ladder” of notes coming due at different times of the year to take advantage of the changing rates.

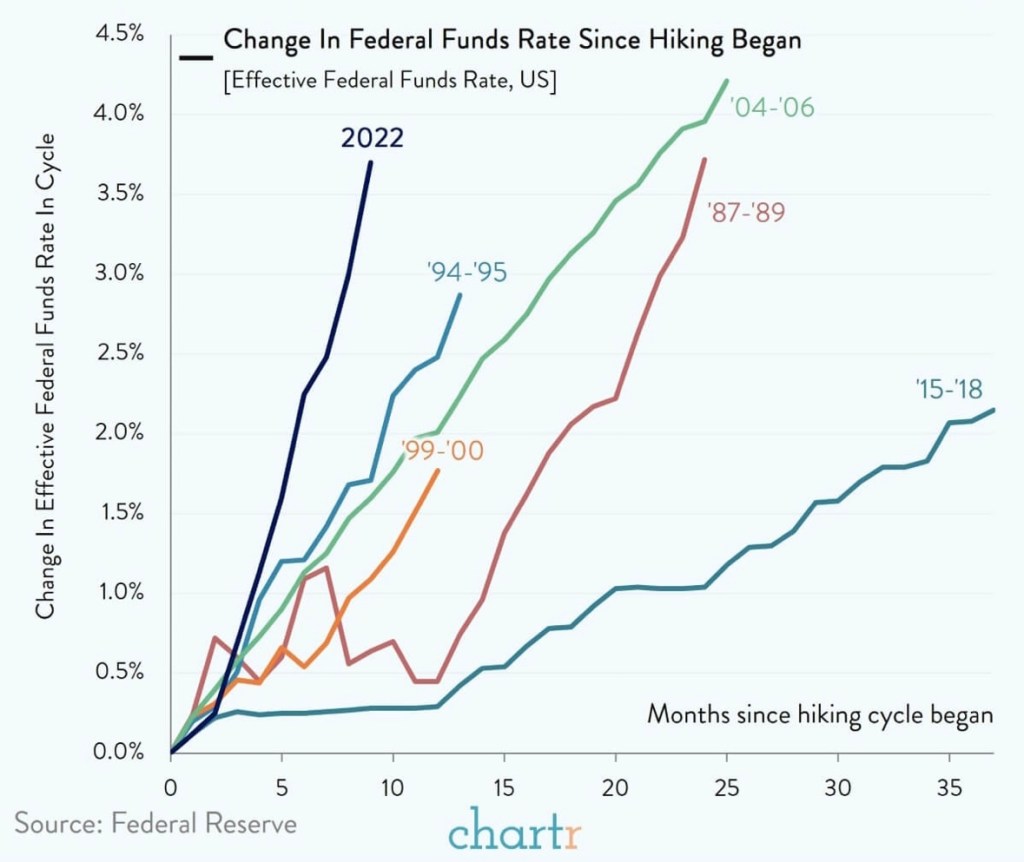

It looks like we are in that situation again. After about a decade of low interest rates, CDs are now being advertised for 4% APY or more. You can see from this Chartr chart how aggressive the Fed has been with rate increases, which have driven CD rates.

The trajectory of the 2022 increases have been much faster & higher than previous Fed moves – and more are likely to come in 2023.

We moved some cash that came free this summer into treasury bills and keep most of the rest of ours in a money market fund that pays 3.5% APY. That’s pretty good right now, even if it is half of inflation.

I also have one zero-interest account with some “fun money” in it that I’m going to try to move into something this week.

Are you back to playing the rotating “rate game” or do you have a different strategy to protect cash from inflation?

Image Credit: Pixabay

Good Morning Mr. Firestation, yes I have recently noticed the big uptick in rates now flowing into old school investment products. Even Money Market accounts are now up to 3.75 and are higher than my “high yield” savings account at Marcus/Goldman. We’ll need to “dust off” the old high rate playbook. “Pay bills right before they are due, keep almost nothing in checking, CD ladders, etc”

LikeLiked by 1 person

Yes – I forgot about waiting until the last minute to pay bills. We usually pay our annual property tax all at once, but we’ll want to go back to paying every 6 months.

LikeLiked by 1 person

We have always maintained a level of cash as sequence of returns buffer and accrued maintenance items and repairs. Over time, this has accumulated to a substantial sum that we shift into the best cash returns available at any given time. For the past year, we’ve utilized a combination of iBonds (currently 6.89%, most recent 9.62%) and a HYS account (currently 3.25%). Let’s face it, they are all losing options to maintain a level of liquidity, as inflation out paces all of these assets over time, but it’s an attempt to salvage as much purchasing power as possible in the short term. I’d love to hear what others are doing…

LikeLiked by 2 people

iBonds … that’s what we moved $$ into this summer! (Otherwise … Just money markets and treasuries for me right now).

LikeLike

My overall dividend yield is 4.63%, and is growing through dividend increases averaging 4% per year. I am currently living on 2.5% of my principal, so I am reinvesting 2.13%. 4% + 2.13% = 6.13%. This is close to matching inflation.

Despite having a portfolio that is flat this year, I have had some winners such as Oil and Gas Majors. Dividend aristocrats like Exxon and Chevron had a current yield that was over 6% when I bought them. This opportunity was caused by Slo Joe taking Executive Actions against the fossil fuel industry. CVX and XOM currently had yields in the low to mid 3% range, so I rotated into other dividend stocks to juice my income.

Selective yield shopping, coupled with partial dividend reinvestments, and dividend increases has kept me ahead of inflation.

I also practice ThomH’s “cash type investments to meet living expenses for a couple years” and Dapo ‘s “pay your bills just in time” cash management.

LikeLike