The simplest route to FIRE (being financially independent & retired early) is to spend less than you make. That is, simply put … to SAVE.

Unfortunately, Americans have never been good savers. I last lamented on this in April 2020, at the start of the pandemic lockdowns. We were told that Americans were such poor savers that the pandemic required the government to bail everyone out by running the government currency printing press overtime.

Link: Our National Savings Dilemma

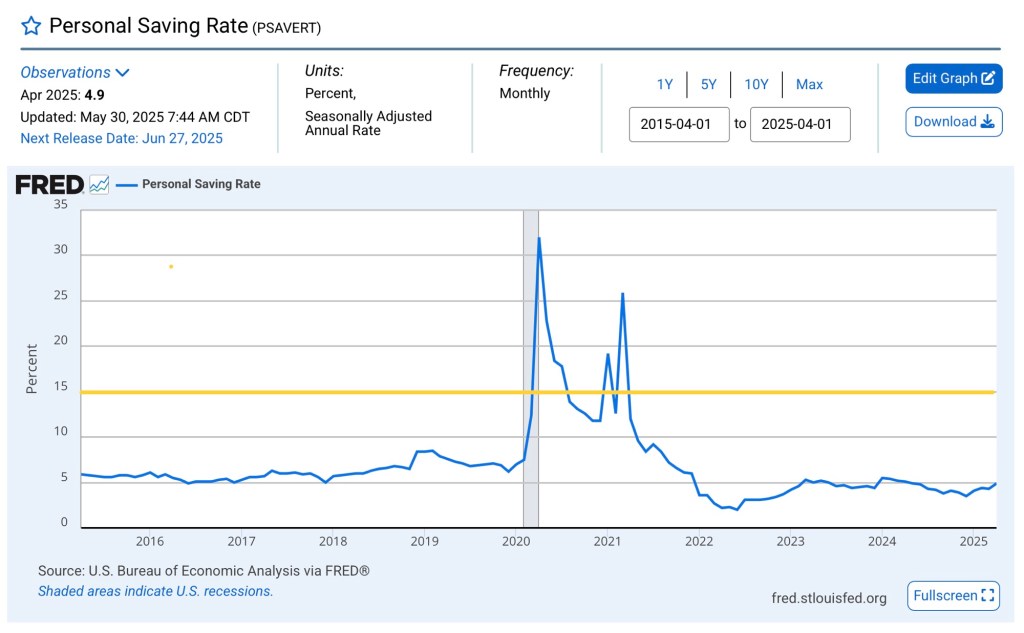

Now 5 years later, I thought I would check in to see if Americans had collectively learned a good lesson and had begun to save for the next rainy day.

The answer: of course NOT!

We’re even slightly worse than before the pandemic …

I’m sure that this will surprise very few readers of this blog. We’ve all gotten where we are – or are headed in the right direction – because we take savings seriously and realize it is the only practical path to financial freedom, independence, and autonomy.

That said, most Americans (67%) are said to live check-to-check, according to a recent survey. Despite the financial uncertainty of the last 5 years, apparently few have internalized the need to save for a rainy day. Sad, honestly.

What do you think would change people’s attitudes toward saving?

Image: Pixabay

If attempted – I think it would take 3 things:

3) Some type of new saving benefit. I haven’t thought this through, but the idea would be to incentivize savings versus spending.

Hope you get some interesting ideas.

LikeLiked by 2 people

With respect to #1, I imagine the financial services companies already spend hundreds of millions a year marketing and deploy tens of thousands of sales people. I imagine almost all of these resources are deployed against consumers already interested in their products.

I imagine #2 would be effective. Scaling back benefits to people who should be able to save for their own would get some action, but no one would vote for it. What if the individual tax savings from “no tax on tips” or “no tax on overtime” were immediately turned into retirement savings?

There are a lot of savings programs now (401k, HSAs, 529s), but utilization is pretty low. About 30% eligible for a 401k do not take advantage of it. I’m not sure what else you can do for people honestly.

LikeLiked by 1 person

People need to become long term thinkers who delay instant gratification in order to become savers. Most people worry about putting on the appearance of being wealthy and spend more than they have coming in.

One of the most important messages in MrFirestation is that someone, especially a couple, can achieve financial independence in a 20 to 25 years timeframe. My wife and I got married in our thirties and the timing worked out that we retired after 25 years.

Once you get people on board with the idea of saving for their financial independence they need to learn to invest most likely in the stock market. They need to see what happens when you compound your money at around the stock market’s long term return of 10% per year. It also shows the importance of starting early.

LikeLiked by 1 person

Helping people become long term thinkers is the answer, but it seems to fight human nature, doesn’t it? Maybe we need to come up with a popular catch phrase to make saving sound cool so that people will mock spendthrifts.

We were a couple years behind you – I worked 27 years, but the last few years were just padding our savings & philanthropic interests. My wife didn’t work outside the home most of those years, either. I think 20-25 years is definitely possible with a little good planning and a lot of spending discipline.

The stock market is the best tool for growing savings, but it still makes a lot of people nervous. I wonder if there is a commercial “savings bond” type product that could be devised to protect people from the downside risk. Something people could buy in small amounts – $100, $500 or $1000 – and it would go up within a safe range. Better than a bond, but easier to use than a brokerage account.

LikeLiked by 1 person

I worked longer than 25 years. The first 25 years after getting married and my wife really pushing for saving is when our magic happened.

Dividend investing changes the way that you look at the stock market. It turns stock investing from being capital gains focused and needing to sell to a greater fool to generate income, into buying an income stream. A really valuable number that most people do not pay enough attention to is that annual income that their investments are throwing off and is the income stream growing fast enough to stay ahead of inflation.

Think of owning a rental property that is providing good income. If lowball investor comes knocking on your front door and offers you 50% of what you paid for the rental property, would you panic and sell before the property goes down further? Of course not.

Look at investing in the stock market the same way. Just because Mr. Market is making lowball offers, don’t panic and sell. Instead look for stupidly priced dividend stocks to add to your annual income stream. Take advantage of Mr. Market, who is an emotional fool who is panic selling. You want to be Mr. Potter in the movie, “It’s a Wonderful Life” and take advantage of others’ emotions to add to your income stream.

Both saving and investing in the stock market require making rational decisions versus acting on your emotions.

I make most of my bond investments through Closed End Funds. You can often pick them up when they are selling at a discount to their net asset value. There are funds focused in specialties such as short term, high yield, utilities, Federal, State and AMT tax free Muni Bonds. These funds are managed by teams that know this space really well and are on the call list of entities making offerings. They pay monthly. The last five years has been awful for bonds because of the inflation during the BiDUMB term, so yields are high right now.

LikeLike