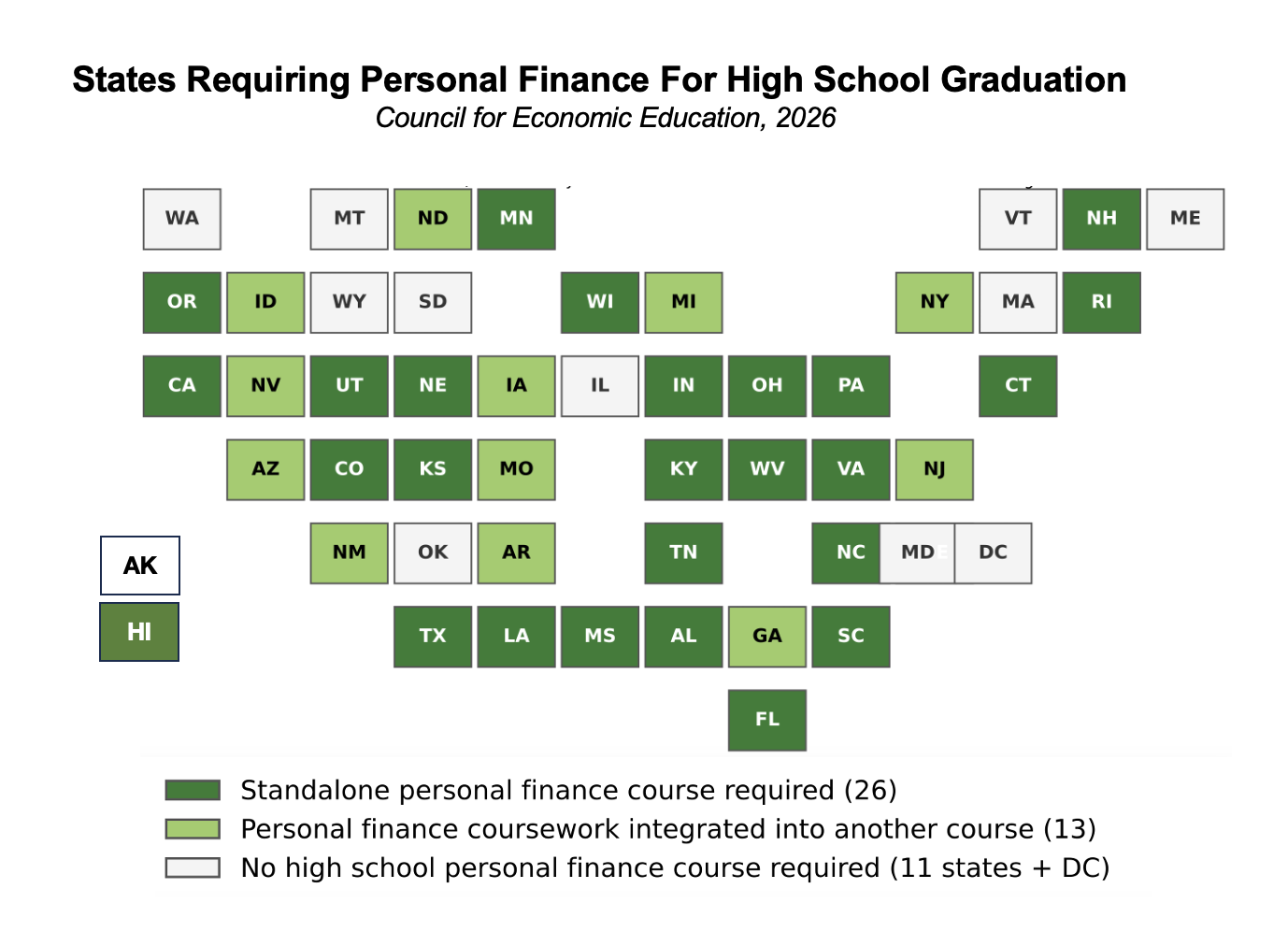

I’m glad to see that public schools are taking personal finance seriously. Thirty-nine states now require personal finance as a high school graduation requirement, either as a standalone class, or integrated into another class, like economics.

For decades, students sat through economics classes learning about monetary policy, supply and demand curves, and gross domestic product. Those topics are interesting, and they certainly help explain how the world works. But when I look back on what would have made the biggest difference in my own financial life, it wasn’t understanding the Federal Reserve. It was understanding my own money.

As someone who retired early, I can’t help but applaud the shift. I was fortunate enough to get a tattered copy of Jane Bryant Quinn’s Making The Most of Your Money from a library book sale when I was in high school. It”s certainly one of the most valuable purchases I ever made!

How different would it be if every 18-year-old understood compound interest, credit scores, debt management, investing, and how to avoid lifestyle inflation? A teenager who learns how a credit card balance grows at 25% interest may save thousands of dollars before turning 30. A young worker who starts investing in a Roth IRA at age 22 has a huge advantage over someone who waits until 32.

Those lessons aren’t theoretical. They’re life-changing.

Economics still matters. Understanding markets and incentives helps explain why the world operates the way it does. But if schools only have room for one course, I’d rather see students learn how to manage their first paycheck than memorize the components of GDP.

The FIRE movement has always been built on financial literacy. The more young people understand money, the more options they’ll have later in life. And options, in my experience, are one of the greatest forms of wealth.

When did you first start learning the ins-and-outs of personal finance?

Image: Pixabay

Great post.

LikeLiked by 1 person

I was fortunate to win the parental lottery with on parent growing their own food during the depression and the other growing up in Canada during the war, which for them began in 1939.

I witnessed them tracking expenses including noting milage and gallons of gas purchased in notebook in car when gas purchased.

I have an early memory of climbing onto Dad’s lap to find the “T H E” letters in the Wall Street Journal, partially how I learned to read.

I also was encouraged to do small jobs mowing lawns, washing cars, delivering papers prior to legal working age.

Debt was always frowned upon except when my father borrowed student loan money at 3% and invested in money markets at 16-18%. Arbitrage on the governments dime.

This was in addition to talking about finances and investing which has been in my area of view forever.

LikeLiked by 1 person

That sounds great. I too had parents that were good with money and passed on their knowledge. My Dad ran a JCPenney Store and my Mom worked at a bank when I was in Hr High / High School. My Dad dud their finances until he was 89, when I took then over for him.

LikeLike

I went to my first two years of high school in Southern Indiana in a blue collar high school. The high school had a required personal finance course that used an easy-to-follow workbook that taught balancing a checkbook, budgeting, filing taxes, and simple investing. The course was taught by a local small businessman who owned a KFC Franchise. This course made a big difference in my life, because my parents were not good with money.

The irony is that my sons went to a Catholic College Prep did not have personal finance. Another father and I approached the principal and suggested adding personal finance to the required curriculum. He didn’t seem to get it, because he was looking for an AP course on the subject. Making something an AP course will surely screw something good up.

Financial literacy could cause graduating students to demand that governments balance their books!

LikeLiked by 1 person

The closest I got to Personal Finance was my brother’s Boy Scout manual (which had a merit badge) and a high school “Business Law” class.

LikeLiked by 1 person