Is it time to rebalance your early retirement portfolio? With the Dow Jones breaking 25,000 this week (I remember when it broke 1,000!) – and after posting 37% growth since the 2016 Presidential Election – maybe it is time to look at your balance of stocks, bonds, and cash and ensure that you have not become overweighted in equities?

The year 2017 was a great year for most investors from start to finish. Our portfolio lagged until the final two months, but finished really strong. They say that the biggest risk your retirement nest egg faces is the market’s performance in your first few years of not working. I’m happy to say that we have had two solid ones so far and are ahead of our FIRE projections,

At the end of the year, we cashed out a lot of stock options that were expiring soon and that helped offset the gains we had in our other stock holdings. Since we didn’t reinvest the money at this point – we kept it in cash – it has effectively rebalanced our portfolio without us spending a lot of time thinking about it. Our cash balances had drawn down to what equals a couple years spending for us. By cashing out those stock options, our cash balance is now back up to about 3 years spending – where I want it to be.

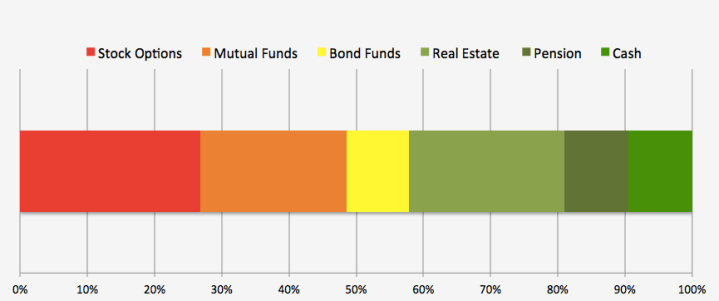

Here’s what our investment mix looks like right now:

My goal is to keep the relatively ‘safe’ stuff – cash, pension, real estate, and bond funds – at roughly the same percent of our portfolio that matches my age. I’m just over 50 now and the yellow/green ranges on the chart almost perfectly match that benchmark.

I’m told by my financial planner that I likely could be more aggressive in investing. Since we are healthy, carry no debt, and have no risk of losing our jobs (we don’t have any!), we could probably tip the portfolio another 5-10 percentage points toward the more risky investments. I see that naturally happening over the course of 2018 as we spend some of our cash.

Some of the strategy here has to involve where you think the market is going to go in 2018. I don’t have any idea, of course, and have seen articles that claim the bull is likely to keep running at the same time other articles expect that a bear is now due to emerge. I will remain cautiously optimistic, but assume the market is pretty fairly valued or maybe tipped to risk after the nice run that we have had. If we could get +5% growth in the S&P 500 this year, I think I would consider that successful.

What do you think the stock market will do in 2018? Are you balancing your portfolio to take advantage of that?

Image Credit: Pixabay

Well, Chief, here’s what I think about what the market will do in 2018: Sometimes it will go up; sometimes it will go down; sometimes it will do neither. My degree of confidence on this is >95%! So, I never rebalance to try to take advantage of what _might_ happen. Instead, I rebalance every year to align with our long-term goals which do not change. I follow three principles to achieve those goals over a 30-year time-horizon: 1) Preserve Capital; 2) Diversify Assets Widely; 3) Maintain Spending Power. Target percentages are set for separate investment categories to achieve our long term goals guided by those principles. Investment categories are rebalanced annually, either up or down, depending on whether we have exceeded or fallen short of target percentages, based on actual annual market performance in any given category. But if I were in your very handsome FIRE boots, I’d focus primarily on exiting stock options in a disciplined manner over the shortest practicable time horizon (eg. 5 to 7 years) because they are a “wild card” for long term planning.

LikeLiked by 1 person

What does your mix from ‘risky’ to ‘safe’ look like? 75/25, 60/40, 50/50. You can see we are about 50/50. The options expire annually between now and 2020. We liquidate them on a steady basis. 2017 was awful on these until the very end. Fortunately, we didn’t need to sell any when they were awful. Back to $60 just today, in fact.

LikeLiked by 1 person

Congrats on $60! Nice recovery. Personally, I’d set up “automatic” schedule to sell, almost regardless of price (except for a “floor”) just to remove from “wild-card” inherent any any individual corporation. Because of 3-decade time horizon, I don’t really think in terms of “risky” or “safe.” All vehicles (even cash) have degrees of unpredictability and likelihood. Most circumstances that determine their final degrees are outside of our personal control. The only things I can control are my goals and principles. My investment advisor calls me “conservative.” I’m fine with that. He can call me anything he likes as long as we stay aligned on my goals!

LikeLiked by 1 person

Congratulations on timing your retirement well! You are right that the research shows those first few years can be very important to your ultimate success, so it seems like you are off to a great start!

I am still a few years away from FIRE, and concerned the eventual end of the bull market could delay things a bit further, or cause unanticipated problems for us in the early stages of retirement.

I was very concerned about the market’s valuation a few months ago, but I think tax reform may delay the end of the bull market for a while. I know underlying business fundamentals haven’t changed, but the E in the P/E ratio for many companies is going to get larger over the next several quarters, making valuations appear a bit more reasonable. There’s a lot of cash around the world looking for a home, and I think market technicals will remain sound.

I think the S&P 500 will be up double digits again this year, despite the bull market being very long in the tooth. If we do see those kind of returns, I’ll look to rebalance investments we will be using sooner (primarily 529 accounts for our children) into somewhat more conservative options later in the year.

But for the record, bowmanifesto’s market prediction is much more likely to be correct than mine!

LikeLiked by 1 person

Double digit growth would be awesome. That markets got a jumpstart on that goal last week, so hopefully that will play out. In addition to tax reform, it is likely that deregulation will also help.

If you carry enough cash into FIRE, it can protect you from the end of a bull market. We carry 3 years spending as insurance. Historically, that would have been a good cushion.

LikeLike

Think it’s smart idea to consider a rebalancing, even if it’s only a little bit. We shuffled our portfolio around too, only have dividend growth shares and real estate at the moment. All ETF’s are gone (but will be rebought of the coming years), winding down crowdfunding and started a very small position in crypto’s (fun money). No bonds for us as we are still in the accumulation phase.

LikeLiked by 1 person

Rebalancing in a strong market is a lot more fun than when the market weak. 🙂

LikeLiked by 1 person

You got that right!

LikeLike

Your decision to retire was very well timed given the market performance. Congratulations! I think the market will continue to be strong again this year (double digit), barring any worldwide catastrophic events, war, etc.. I do believe the macro economic effect of the tax changes will help drive some of that performance. I personally alway ignore the market and rebalance every January, so I did it last week. Occasionally, I may do it during any given year, like this past year, when there are large swings that warrant rebalancing sooner (like a 5% swing in any specific investment area). I’m a “lazy” index investor (along with being a “not so lazy” real estate investor). I tend to think of my retirement in three phases. Phase 1: now (age 52) until age 60, which I entirely fund with real estate cash flow. So I guess this phase would be considered invested very conservatively in all real estate. (Along with some substantial cash reserves). Phase 2: Age 60 to age 70 will be covered by a combination of real estate cash flow (50%) and (50%) 401k & Roth IRA funds. Over all it will be very conservative as I tend to think of my 401k & Roth IRA funds separately from my RE investments. But the 401k & Roth funds are invested 70% aggressively and 30% conservatively (slightly more aggressive when considered singularly or separately from my real estate investments). But overall, the math says I’m very conservative because the 30% conservative portion of my “more liquid” investments (in the 401k/Roth) is in reality on top of the real estate, so over all I am actually only 35% aggressive and 65% conservative (because of my large real estate position). Phase 3: Age 70+ will be similar to Phase 2, but will (by then) include SS payouts, which…when thought of like a pension, will make me even more conservatively invested overall. But I will likely always stay somewhat more aggressive within my “more liquid” accounts because they become less necessary. So that’s my diversification story.

Cheers to another (hopefully) great retirement year in the market!

LikeLiked by 1 person

Yes – cheers to another great year for both of us, Thom. I am also a ‘lazy index fund investor’ for the most part. When you retire early, people think you had some amazing investing success to get there and they always seem surprised to hear that boring index funds work.

I like the way you have your ages and income sources worked out. I do think in terms of three buckets/horizons, but I have never spent the time to designate what would be spent when. If market returns like these continue, it might be an easy exercise!

LikeLike

Yes, I hope so! I always tell my two daughters… It’s not always about making a huge salary (although it certainly doesn’t hurt). It’s not about being the smartest market analyst (although it probably doesn’t hurt if you are). But if you can be persistent, don’t make stupid mistakes, and start early enough…anyone can become FI at a relatively early age. Fortunately, they are both off to great starts themselves!

LikeLiked by 1 person

Hi – Curious in your RE allocation and long term plans related to it? That is one area that I struggle with a little given the recent appreciation of my small 4 unit and has me contemplating cashing out – values are at a level that I was not expecting for at least 5~7 years from now. That would throw a monkey wrench with my plans, since I was factoring in the monthly cash flow it produces to help cover expenses. Enjoy the blog..!

LikeLiked by 1 person

I don’t have our assets cleanly plotted out into years, but conceptually employ a three horizons/buckets approach. We live off stock options now – some expire every year. We hold cash to act as insurance in the event of a downturn. And everything else ip- outside of our house – is roughly 60/40 equities & bonds.

LikeLike