I think we’ve made it! The biggest concern that most early retirees have is how they will manage the cost of health insurance between leaving MegaCorp and gaining retiree benefits or Medicare eligibility. It’s a topic I’ve provided many updates on over the last 5 years because health insurance is an expensive and dynamic market.

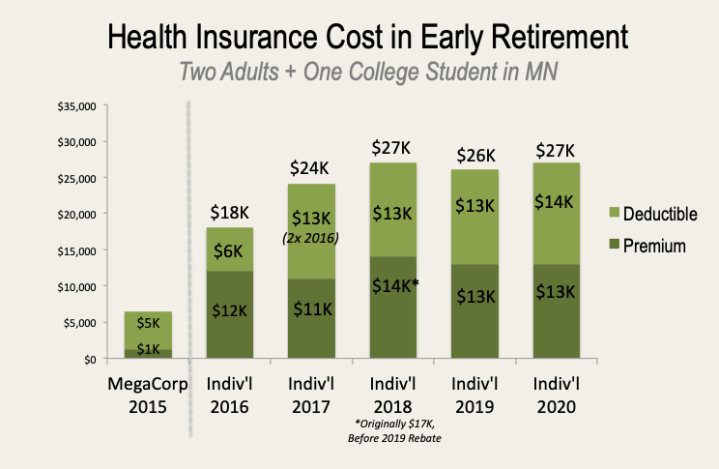

This is the last year of open enrollment where we will pay 100% of our own premium before we reach MegaCorp retiree benefits. I’m not thinking those are going to be especially generous, but anything would help. Here’s the history of where we have been in terms of coverage & cost …

As you can see, at first our deductibles doubled (2017) and then our premiums shot up about 50% (2018). This year (2019) brought welcome relief on the premium (and a $3K rebate on 2018) and it looks like next year (2020) will be about the same as this year. It looks like our deductible creeped up, but it’s really just a rounding error from $13.3K to $13.6K. I’m fine with that relatively small change.

Next year will also bring the financial benefit of our son graduating from college and getting off the ‘family payroll’. He interned at a company last summer and accepted an offer for full-time employment with benefits, starting next summer. I’m guessing our premium will drop by about 20-25%, or $3K on an annual basis once he goes on their plan.

I should note that while the most unexpected jump in the chart above has been the doubling of our deductible, we’ve stayed in good health and have paid very little out of pocket ourselves. I was talking to a friend recently who had some treatments for skin cancer that topped $45,000. That quickly filled up his family’s whole deductible for the year. While we created our FIRE budget with enough money to cover our whole deductible, we’ve been fortunate to not spend much of it, except some very small things.

How is your Health Insurance Coverage looking for 2020?

Image Credit: Pixabay

Towards the leanFIRE side of things, there’s this lovely little income spot in Illinois between 28500 and 32000 MAGI with a family of 3 where ACA insurance is $100/month for two adults on a nice PPO plan with a $50 deductible and a $800 out of pocket maximum. Literally the same plan I had while employed even. Kid is 100% free for all costs on CHIP.

Actual withdrawals and spending was over $50k and I even had room for a little Roth rollover action!

LikeLiked by 1 person

That sounds like quite a bargain, but requires some finesse in managing your income just perfectly. We have stock options to sell each year through 2022, so that keeps our income much too high to even think about subsidized ACA health insurance.

LikeLike

We also play the ACA subsidy game. We will have the same Anthem Bronze-HSA policy in 2020 as we had in 2019. The policy premium actually dropped about $100/yr, but the subsidy was also cut by about $1300/yr. So our net subsidized premium payment rose approximately $100/month for 2020 for the exact same policy (slightly higher deductible and max out of pocket). I’m not complaining, it is still a great deal for an early retirement health care coverage option.

LikeLiked by 1 person

The ACA has certainly been a boon to many early retirees. I’m always surprised they didn’t put a ‘wealth test / limit’ into qualifying for the subsidized benefits.

LikeLike