If you’re not familiar with the name Bill Bengen, you probably are familiar with his work. Back in 1994, he published his Trinity Study suggesting that a 4% withdrawal rate of retirement savings would be ‘safe’ for most retirees, based on historical financial returns.

Bengen – now long retired himself – has been in the news updating his thoughts on the ‘4% Rule’, as he does now and then, and the news is good. He now believes – based on additional work by Michael Kitces – that the ‘4% Rule’ is too low and most could plan on a 5% figure, or higher, over the long run.

His updated thoughts (LINK) are formed by changes in the market from the original data that he used. The ‘4% Rule’ was largely based on weak market returns and high inflation in the 14-year bear market of the late 1960s and 1970s. We haven’t seen that profile in decades, he argues, and are probably oversaving.

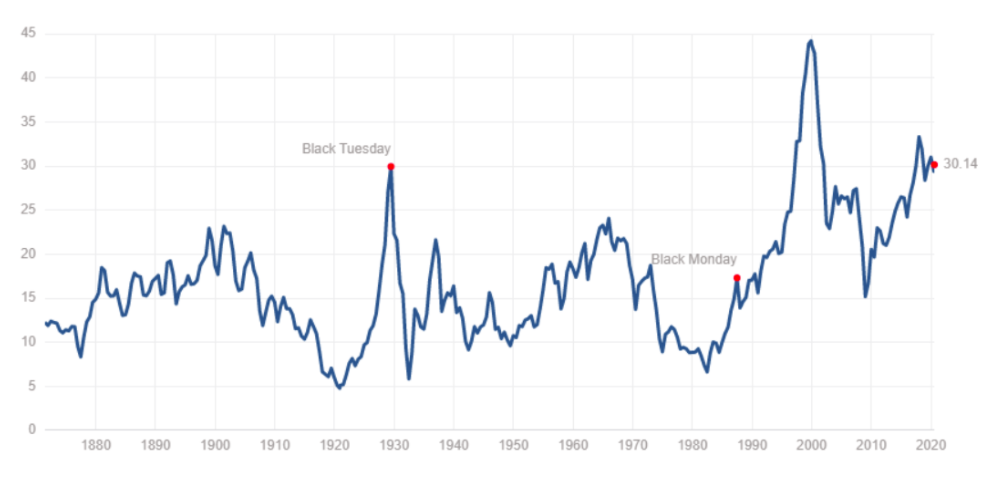

Bengen calls his maximum safe withdrawal rate ‘SAFEMAX’. In the chart below, he shares his analysis of SAFEMAX with the Shiller CAPE, which is a measure of S&P 500 price/earnings ratio. The chart ends in 1990, because that represents a 30-year retirement span to 2020.

You’ll notice in the chart that periods of low stock market valuation (in the orange) correlate with the opportunity for higher SAFEMAX spending (in the blue). The blue line has actually never gone below 4.4% – that’s what made it ‘safe’. The chart goes all the way back to retirements starting in 1926 and the average safe withdrawal rate is 7%.

The chart shows that retirements that started more recently – between 1974 and 1990 – have enjoyed a SAFEMAX hovering around 8%. That’s an incredibly high number. Those folks have enjoyed a wonderful environment for their retirement financials, but who knows how quickly the financial environment might change?

Going forward, Bengen’s read of the data is that when the Shiller CAPE is above 20 (‘overvalued’), a 4.5% SAFEMAX works. When it is below 20 (‘fair value’), then it is appropriate to increase it to 5.0. If the PE dropped really low – below 12 (‘undervalued’) – one might choose a SAFEMAX as high as 5.5%.

Those changes may not seem like much, but even half-percentage point changes in your retirement withdrawal rates are pretty big. He also suggests SAFEMAX adjustments for different inflation rates – dropping SAFEMAX by 0.5% for every additional 2.5% in inflation.

So where do we sit now? Inflation has been low, but unfortunately the Shiller CAPE is extremely high right now. It broke 30x in 2020 and the outlook for further S&P 500 price growth would seem to be extremely limited.

Shiller ‘Cyclically Adjusted Price/Earnings Ratio’ – 1870-2020:

It’s for that reason that we are not changing our SAFEMAX number (close to 4%) despite Bengen’s solid analysis. The market’s ‘Trump Bump’ (up 55% since November 2016) doesn’t seem to have been carried by corporate fundamentals. One could argue that it will take years of corporate earnings growth – with no change in stock prices or inflation – for the S&P 500 to be fairly valued.

What expectations for SAFEMAX have you built into your FIRE Plan?

Image Credit: Pixabay

One area that has received almost no ink is the impact due to “fear that you are not investing enough for retirement” and the forced retirement savings programs placed upon low wage workers. Both impact vast sums invested in the market and vastly exceed draws from retirees.

An example is my 24 year old. He worked part time for his university for two years and guess what? He has a retirement account with $450 value. This is an unexpected benefit which will pay huge sums in forty years. I told him to convert to a Roth IRA and I will pay the tax for him as a gift. Compounded this should be about $25,000 at that point and he never contributed a dime.

LikeLiked by 1 person

Dave speaks wisely. A kid that age with that amount – convert to Roth. As for me — a ‘SAFEMAX rule’ , at 4, 4.5, 5%, whatever – may be a reasonably rough guideline, but also can be needlessly burdensome. Rather, I suggest — also mix in a bit of REALITY! Just take what you NEED and leave the rest. Just like in “The Band” ‘s song……

LikeLiked by 1 person

The less we focus on what we ‘could’ spend, the less we seem to spend. I don’t have a monthly budget – we just look at how we are doing overall a couple times a year. This year – despite the pandemic – looks good. I’m sure our spending is WAY down without travel, concerts, and shows due to CV19.

LikeLike

Agree! My son’s company has the deal where everyone is ‘automatically’ enrolled in the 401K. That’s great. He’s 23 and also has a Roth with $ in it that he earned working in high school and summer jobs. I started saving at age 23 – he beat me by starting 5 years earlier.

LikeLike

,,, and he beat me by starting 8 years earlier. Not generally a fan of must-opt-out plans, but “Forced” 401k/403b programs are a NET benefit that take ….ahhh….arguably……. ignorance etc out of the equation, esp for young people

LikeLike

I’m fine if a private company puts everyone in. I wouldn’t be if it was the government- but that’s my political hang-up, I guess. 🙂

LikeLike

Great to read about the optimistic side of this rule. Normally you only read about the doom and gloom how 4% is not enough and too dangerous and never designed for longer retirements. My thoughts were 4% is enough and there is ability to adjust during the first years to prevent the risk of bad returns in the first years of retirement.

LikeLiked by 1 person

We built our plan on about 4%, but I haven’t tracked our actual spend too closely.

LikeLike

We built our FIRE plans around an initial SWR target of 3.41%. When we do begin to draw from our retirement accounts, however, we will likely utilize a dynamic SWR based on market conditions (likely using the Shiller P/E ratio to determine adjustments). We have been early retired for 3.5 years now, and also utilize a similar dynamic allocation for our portfolio diversification decisions. Dynamic SWR’s and allocations were initially outlined in Micheal Kitces blog and further discussed in a series of detailed blogs by Big ERN…for anyone curious about the dynamic theory. His SWR Series is a great read. The above information is great news considering the massive disinformation (lately) calling for much lower SWR’s from some bloggers like Sam over at Financial Samurai. I will likely stay conservative, as we hope to not really rely on our retirement accounts to a large degree.

LikeLiked by 1 person

I have to say 3.41% is very exact! Do you have a regular process to withdrawal that amount in to savings, or do you do what we do – just transfer out some money when you need it and only worry if you need to start taking out more?

LikeLike

So we have been retired 3.5 years now and are still not drawing from our market assets. I may have mentioned before that we “early retired” entirely on rental real estate investments. We have over fifty rental units, that (fortunately) provide cash flow to more than meet our current needs. We are still four years from the magic 59.5 age to begin drawing from retirement assets. I developed our allocation and safe withdrawal rate plan based on a convergence of many models, but as mentioned above, the biggest influence is from the theory’s outlined by KItces and Big ERN with my own specific twists based on my own risk tolerances and experiences.

To more specifically answer your question, my personal investment plan outlines in detail the withdrawal process, but here is a short description. Mentally, the monies are bucketed into short, medium, and longer term needs. Like the typical three bucket theory, short term in cash (3 yrs), medium term in bonds/etc (7 years), and Long term (10+ yrs) in equities. In a year where equities are up, rebalancing comes from the long term bucket to refill the others. If equities are down and bonds are stable, the rebalance comes from bonds. In a year neither stocks or bonds are up, we either simple draw from cash or cut back spending to rely strictly on rental income. So yes, we will setup an annual rebalance to a high yield savings account (cash) that is then drawn from monthly to refill our “spending” checking account. The same process is used for rental incomes currently. We own multiple LLCs that monthly kick off cash flow to the same high yield savings account, which provides a salary to our personal checking account. We will simply get nice raises at the age of 59.5 (when there are no longer penalties to draw from retirement accounts) and again when be begin drawing Social Security. I hope answered your question, and sorry it was long winded.

LikeLiked by 1 person

Great explanation! We have a ‘loose’ three bucket approach. Our cash bucket has come from stock options we have had to exercise each year. Going forward, I like the idea of taking $ from the most favorable bucket available based on the market valuation at the time as you are doing.

LikeLike