Well, it looks like “the Boy” – our seventeen year-old son is set for where he wants to go to college. I’ve written before on the cost of college, but wanted to share a little bit about how we have saved & planned for his matriculation into post-secondary education. Many people can’t conceive of retiring before your kids are done with college, but I feel confident that we are well set in that department. How did we do it?

When my son was very little, we went to a weekend work event as a family and my boss told me “start saving for his college now!” The boss had three boys in college at the time and he said he had wished he had saved much earlier. Our son was probably only about three years old at that point. Before he turned four, we started a 529 account and were very diligent about putting money in. As you probably know, money in the 529 plan grows tax free as long as the funds are used for college expenses.

We chose the 529 plan in a neighboring state, where my parents live. Their state had a good program and if we gifted my parents some money, my Dad could make the 529 contributions and take a deduction on his state taxes. Worked well for everyone.

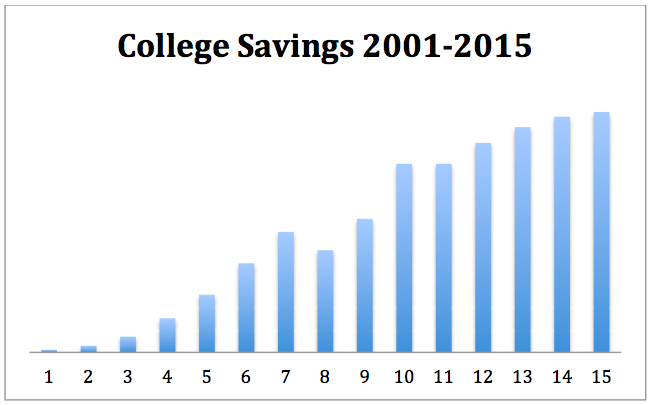

It was tricky to know exactly how much to put in the account for him. We looked at college costs for four kinds of schools in progressive order of cost: small state schools, large state schools (Big Ten), smaller private schools, and nationally known private schools. My wife and I attended a small state college, but we wanted ‘better’ for our son. At the same time, I didn’t see him likely heading off to the Ivy League, Notre Dame, or Stanford (long odds). So we decided to save enough that he could go either to the big state college, or the local private university. With only one child, you don’t want to deposit more into the 529 than you will use (although it can be used for grad school or transferred to a cousin). This meant saving about $2K a year when he was small, $4K when he was in grade school, and up to $8.5K when he was in junior high. The good news is the money built up quickly and we haven’t made a single additional deposit to the account since he started high school, and the account is close to $100K now.

You can see how quickly his 529 account ramped up. In the last fifteen years, we only saw one down year, which was 2008 when the stock market fell so dramatically. I haven’t messed too much with the risk profile of how the money was invested. Early on I chose one of the “age adjusted risk profiles”. That means a good portion of the money is invested in bonds at this point.

The school he wants to go to is pretty expensive – the official price is about $45K a year (tuition, room & board). That said, there is a lot of financial aid available – based on the students’ grades & ACT scores – even for families that are pretty well off. Our son is a good student (not great 4.0 GPA, though) and got a very good score on his ACT Test. He also has done a lot of activities, service work, and some athletics, so that should help.

Based on the “College Cost Net Calculator” that they have on their website, our son would qualify for almost $20K in aid. Most of it is a pure “merit gift”, with a smaller percent available as low interest loans or work study job pay. We won’t want him to take out loans (although the work study is a good idea), so the $25K-$30K a year we end up paying out for him will almost completely be covered by the amount we have saved in the 529 since he was little. Since we currently pay tuition for him to go to a Catholic high school ($13K/yr), I think our cash flow will actually get better once he goes to college as his 529 balance is withdrawn.

College is certainly a daunting expense. Not many families look at a six-figure amount for anything more than the family house in their entire lifetime. I’m glad that we started saving early and appear to have the hurdle cleared. It would be hard to think about retirement at my age, if this major cost wasn’t taken care of.

How are you thinking about college costs relative to your goals for retirement?

Once again, you astound me on your pre-planning thinking. Congrats on your son deciding where to go; I know from friends that is a momentous occasion.

LikeLike

Thanks so much! 🙂

His 18th Birthday is this Friday.

Very exciting time.

LikeLiked by 1 person

Nice work saving up over all those years! Great that things are lining up so well for your son to have his college paid for! We don’t have kids and are thankful we don’t have to worry about this expense! Although it also means no one will be looking out for us when we’re old and grey, so… trade-offs. 🙂 I think it’s smart to have him do work study to pay for part of his education — he’ll be earning dividends from it for his whole life, so makes sense for him to invest in it! And I think if he took out some small loans, that’s not the end of the world either. I had about $10K in loans at graduation, which was only a $100 a month loan payment. It helped me think about how to deal with debt at a young age — namely, that I hate debt — and made me appreciate my education in a different way. I’m not advocating for debt, but if it’s the best option and his obligation is ultimately small, it’s not super evil. 🙂

LikeLiked by 1 person

Kids who take care of you when you’re old… I’ve seen examples of them, but working as a nurse’s aid while in university, I’ve also seen a lot of old folks who never got a visit anymore from their children. Or maybe once a year at Christmas. So: don’t depend on your children to help you when you’re old! Instead, I would say: save up some money yourself, and try to stay involved with the local community and friends, so that they may be willing to help you out here and there when necessary, or just will be happy to come and visit you.

LikeLike

It’s best to have your own plan then oblige your kids anyway…

LikeLike

Great post. I have a 17 year old too and we’re working through this right now. Used 529 Plan too but you started much earlier. 🙂

LikeLike

Earlier is always better to start saving… Funny thing is, at the time I thought we were starting late.

LikeLiked by 1 person

I am very much looking forward to hearing how it went with the withdrawals of 529, etc. and the overall experience of having the kids leave the nest. I am not sure how we will react, I got teary dropping one of in kindergarten this week lol.

We are super funding 529s to 25k each (so that we take most advantage of tax free growth) and we had planned to then add a little more there each year to have about 100K for each, but then decided that we will leave it at 25k by end of yaer for both and then put aside about 100k total in post – tax brokerage accounts by the time college arrives, fund the rest via their work-study and our work (at least first, we want to retire as soon as second one goes off). It is so hard to predict how much college will cost, what it will even look like in a decade + (esp given how unsustainable it is becoming and ROI is just not as clear cut in some cases) and who knows if they will even want to (or can) go to college. That is how we are hedging our bets then….it all else fails we can give to them to do as they wish – even with 10% penalty to travel or do use as estate planning for their own kids education if they ever have one…

LikeLiked by 1 person

We made filed the online ‘paperwork’ to make the first university payment this week. The money gets wired directly to the school. We saved about 90% of what he will need in the 529, so we shouldn’t have extra.

LikeLiked by 1 person