Before I left MegaCorp last year, I had the chance to speak with a room of 20 of our newest MBA recruits who were in a leadership development program for the company. While I was wrapping up my career, most of them were just a few years into their career.

I was giving them an update on a digital marketing initiative taking place across the company, but they were quite interested in how I had managed to become financially independent & retire early (FIRE). I then shared with them a simple rule of thumb that I will share here: if you save half your income, you should be able to early retire in just 20 years.

Most people are surprised to hear that if they start working at age 19-22, you could be living a life of leisure by age 39-42. When the world tells you that you’ll need to work until 60-65 to retire, the idea of hanging up your career decades earlier comes across as a bit of a shock, but the math is pretty straightforward:

You can debate the rate of return or what is a safe withdrawal rate for an early retirement, but the math is pretty straightforward. I plugged in $50K for a year one pay – average for new college graduates, or median for a plumber – but, the starting pay doesn’t really change the math.

The model assumes 4% annual raises on that pay and spending only 50% of what you take home. I assumed a 7.5% ROI on saved income – about 2.5 pts less than the S&P 500 long-term average – a rate that can be boosted with company or union matches on retirement savings.

The framework certainly would require lifestyle sacrifices (particularly early on), but plenty of people have websites that focus on frugal living that millennials have made trendy. Doubling up in housing, using public transit, and other money-savers can make a big difference early in your life. Getting married and living on just one income is another strategy that people use. And, the model doesn’t account for pay raises from promotions that could be invested in housing, education, or other ‘extras’ that have lasting value.

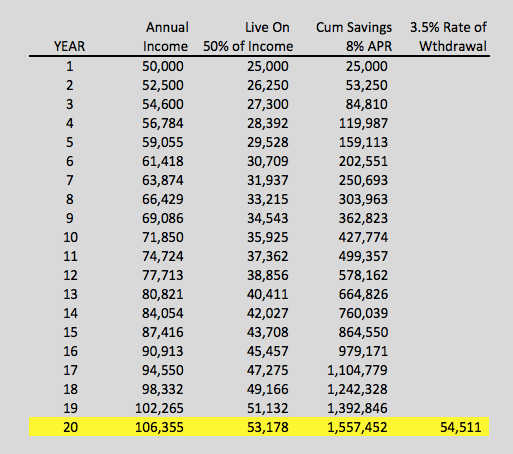

Additionally, just a few more years worked – make a huge difference in the model and “buy” you a significantly enhanced retirement. If you can make it in just 20 years, perhaps 25 years of working (to age 44-47) doesn’t seem to difficult.

Here is what 5 more years does to the model:

Now your rate of withdrawal is more than 40% higher ($92K / $65K) above the lifestyle the saver has been living on. That either buys more security on your withdrawal rate, or gives you a super retirement.

In the end, I hope you see that early retirement may require sacrifices, but it is not complicated. As Dave Ramsey says, “you have to live like no one else if you want to live like no one else.” MrFireStation worked a leisurely 27 years before retiring at age 49. If you are just starting out, you should set your savings goal high!

Image Credit: Pixabay

Not to complicate the model, but salary generally increases more (on a percentage basis) early in your working career than later on. Which is good a thing, as you’ll ramp up your total savings more quickly, if you’re living on 50% of that amount!

LikeLiked by 1 person

Agree – you could probably build a 15 year model to retirement with promotion pay increases. Just tried to keep things simple.

LikeLike

I don’t remember the exact numbers, but in a previous role (~1999) I worked on some retirement planning software. One thing we realized, based on some data sets from the Department of Labor, is that salary increases over the course of a working career are usually not linear. The biggest percentage bumps come in the first decade, followed by smaller raises for the next 10 years or so. For most workers, once they reach their 40s, their inflation-adjusted salaries are essentially flat for the remainder of their working years.

So we created a “salary curve” for our model and found that the predicted ending retirement balances were approximately 25%-30% more when using this assumption, as opposed to steady increases each year. (Assuming the same starting and ending salary amounts.)

LikeLiked by 1 person

Interesting. And if people are very good savers, they could FIRE even before their salaries flatten out!

LikeLiked by 1 person

Good post. I ran my numbers again from when my wife and I got married in 1994.

We did exactly what you suggest living on one paycheck and saving and investing the other. We had a couple years of windfall earnings between 1996 and 2000 were we saved and invested an estimated 2/3rds.

After 2000, we maxed out two 401-Ks including the $6,000 catchup provision, which amounted to around 25%. There were a couple years both of us were not working, so we couldn’t max out every year.

We retired after 26 years of following this investment program and now I know from the 4% rule we could have retired 5 years earlier. It would have been tight, but when we retired our budget had a huge margin of safety built in because we could live on a higher income than we had working with only a 2.75% withdrawal rate. Our dividend and fixed income investments became so high that we were making several times the income we made from working. That is when we decided to retire.

Here is something for young couples to think about. The money and the excess windfall that we socked away during our first six years had more time for compounding to work its magic. The last ten years was less than 20% of the overall amount we had saved up. The savings you make when your are young and think retirement is far off, will be the bulk of your financial independence. Those newlywed savings are the most important.

LikeLiked by 1 person

Agree – time plays a HUGE factor! If the formula is principal x rate x time, people seem to undervalue the time element. We too had ‘over saved’ by the time we were in our late forties and were making more from investments than working. Yours is a great case study for younger people to see.

LikeLiked by 1 person

This is the strongest message you have because it makes reaching FIRE status not seem so daunting. What you are offering sounds more appealing than what the likes of Kiplinger’s is offering. Twenty years does not sound as bad as 45 years with part time work to extend out the time to claim Social Security. Let’s call this plan the 45 and 5 plan, while yours is the 20 Year Plan.

In our cases, the extra five years we worked to have a richer retirement wasn’t the same as someone who is living paycheck to paycheck. It feels better knowing you can walk away whenever you want and the only reason you are working is to afford yourself a better retirement.

I already got my son started on this sort of program at age 24. It actually works very similar to the 20 year pensions that the military is offering in terms of timing, but pays much better.

You were in the marketing game and this seems to be an underserved market because most companies offering retirement plans are offering the 45 and 5 version because they don’t want to offend people by telling them to stop wasting money.

LikeLiked by 1 person